Suhani Adilabadkar

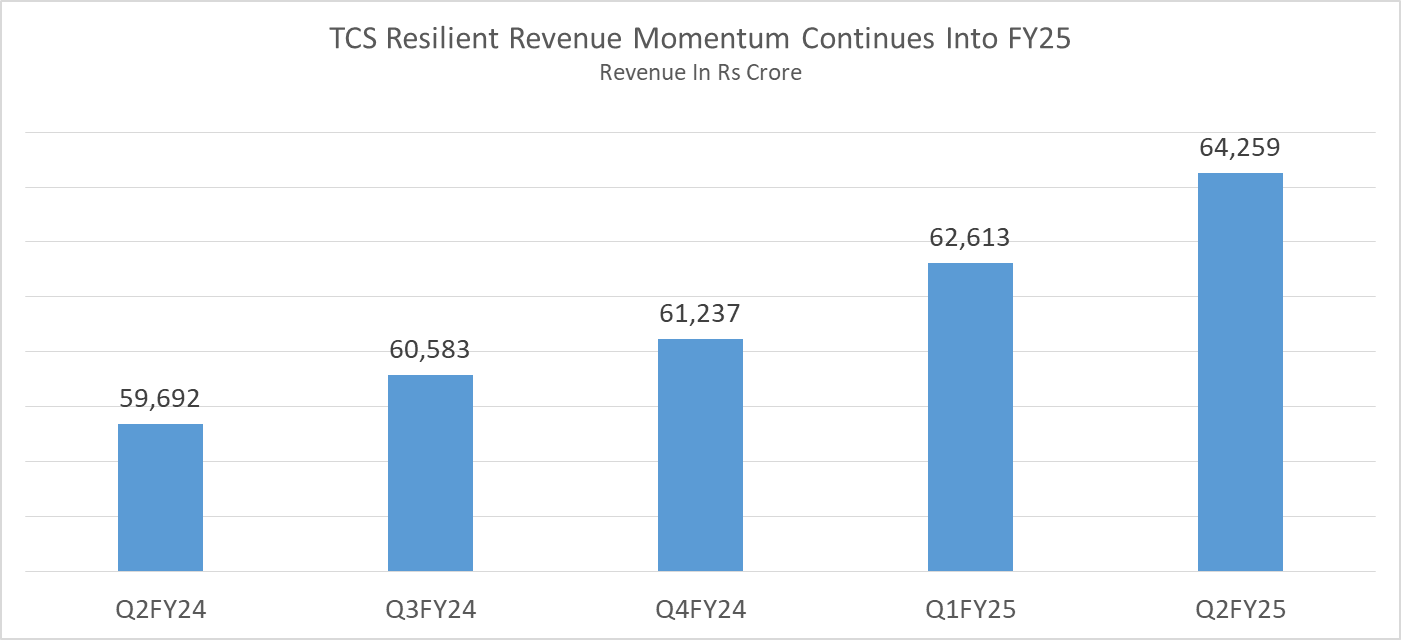

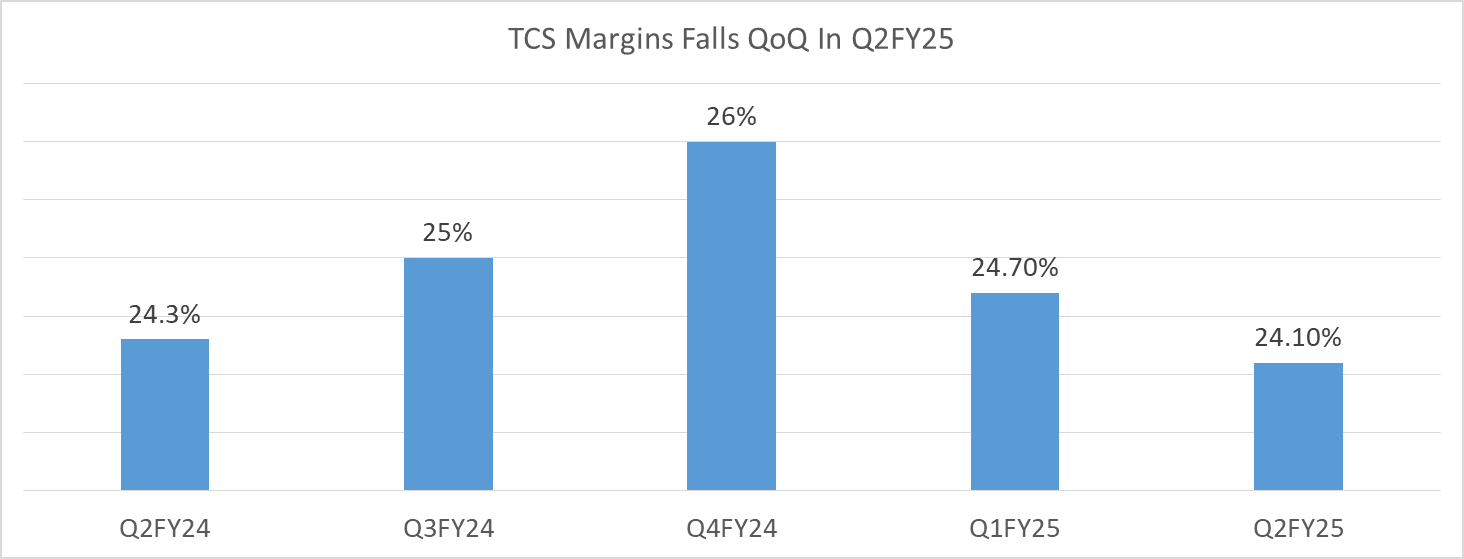

Tata Consultancy Services (TCS) reported stable results for September Quarter 2024. The IT major remains resilient amid weak demand, slower decision making and lower discretionary spend by clients. While revenues at Rs 64,259 crore grew by 7.6% YoY, margins slumped 60 basis points (bps) sequentially and 20 bps YoY.

Operating margins at 24.1% were impacted by higher sub-contractor expenses in September Quarter 2024. In dollar terms, revenue stood at $ 7,670 million with a YoY growth of 6.4% in Q2FY25.

Speaking on September Quarter 2024 results, K Krithivasan, Chief Executive Officer and Managing Director at TCS said, “our diversified portfolio and early investments in growth markets are bearing fruit. All the growth markets continue to grow above company average. However, as a general trend in the major market, the demand outlook continues to remain cautious, as seen in the last few quarters.”

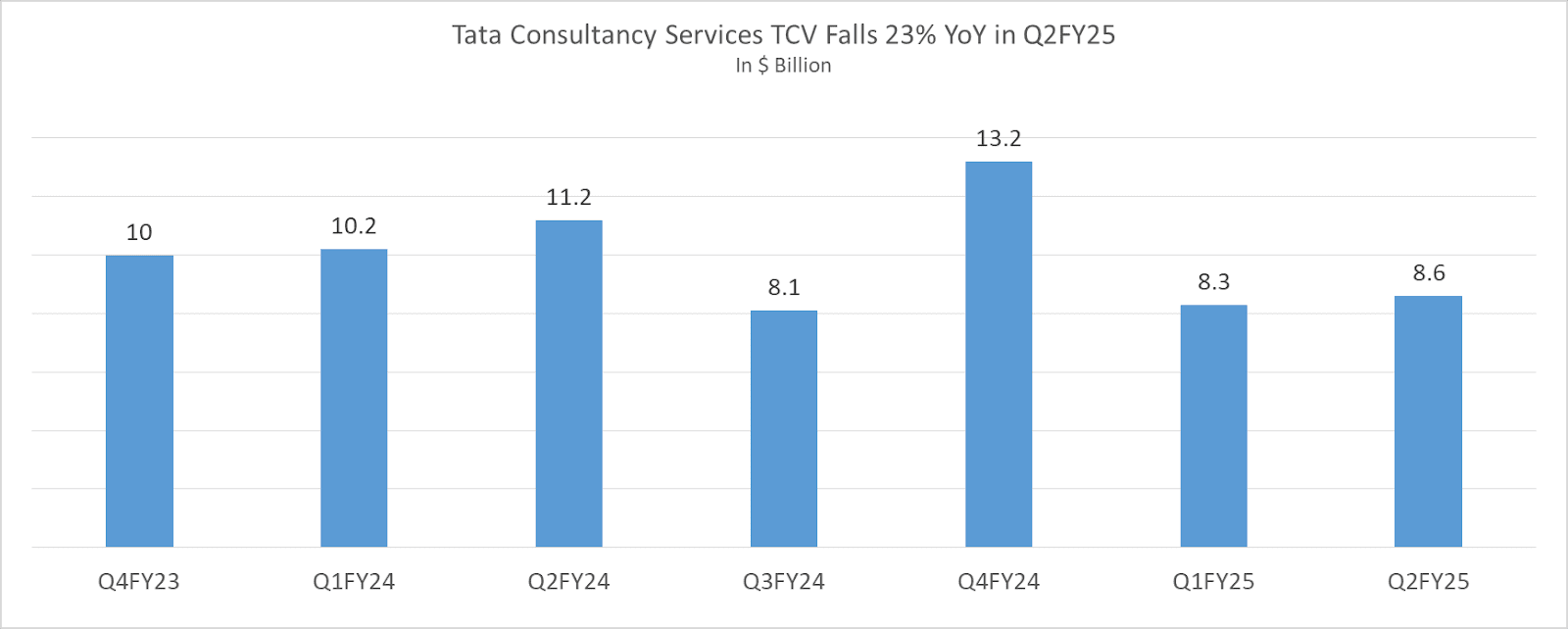

Total Contract Value falls 23% YoY in Q2FY25

Tata Consultancy Services reported total contract value (TCV) of $ 8.6 billion in September Quarter 2024. TCV or order book indicates growth potential in the near future. According to the management, TCV in Q2FY25 is incomparable to corresponding quarter previous year, due to absence of mega deals. There were mega deals worth $ 2 billion in Q2FY24 previous year. On the TCV front, Krithivasan said, “This year, we had somewhere between close to 16-17 billion in TCV in H1FY25, with some large deals coming in and with all the better deal closure, we may be closer to the mark than we were last year or if it is lesser, will not be less by a big number.” In FY24 overall TCV was $42.7 billion, a record growth of 25.2% YoY. The banking financial services and insurance (BFSI) TCV stood at $2.9 billion and consumer business group TCV was at $1.2 billion. And the TCV of deals signed in North America stood at $4.4 billion in September Quarter 2024.

Client Specific Challenges Impact North America Growth, BFSI Looks Stable

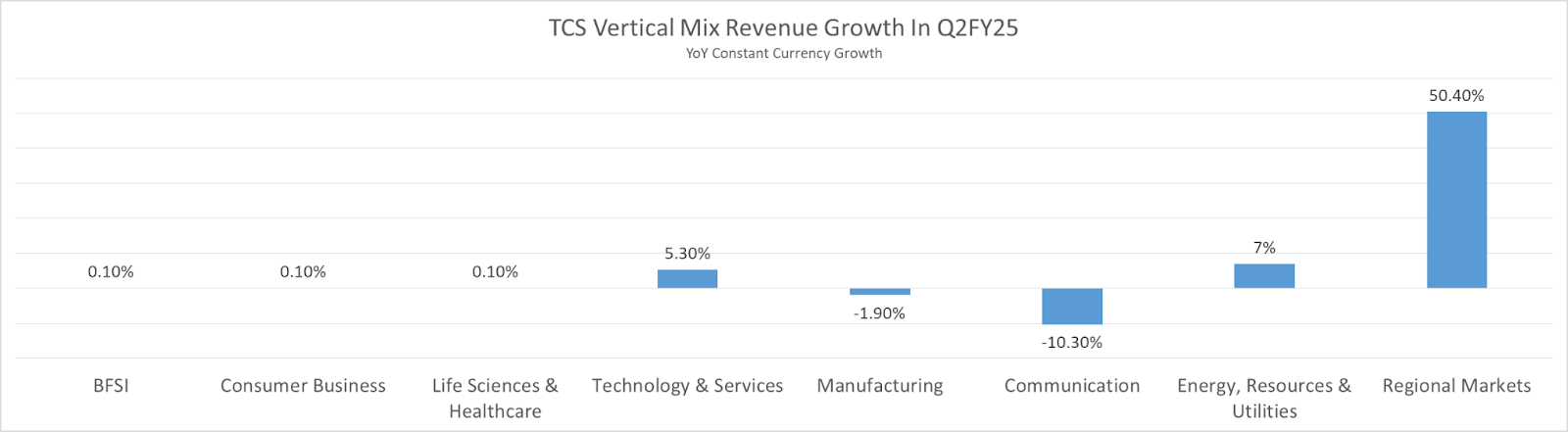

BFSI vertical returned back to positive growth after four quarters in September Quarter 2024. While the company is yet to see large transformational deals in its biggest vertical, the management is positive about BFSI growth. Speaking on BFSI vertical, Krithivasan, “In BFSI, financial institutions in the US are looking at sustaining the growth momentum with the Federal Reserve’s first interest rate cut in four years. Stability in the macro brings initial signs of confidence. With the easing of interest rate environment, consumer confidence and industry confidence will get better. This can potentially lead to improved investment.” The next big vertical, retail or consumer business also reported positive growth of 0.1% in Q2FY25 after three quarters. Consumer spending in the upcoming holiday season is expected to play a crucial role in determining client budgets towards transformation initiatives. While BFSI and retail seem to be on the growth path, manufacturing and life-sciences growth fell in September Quarter 2024. Manufacturing business has been impacted by supply chain and labour challenges. Elaborating lower growth in the manufacturing vertical, Krithivasan said “labor issue is around aerospace. Supply chain issues are in auto as well as aerospace.” Coming to the life sciences and healthcare vertical, the company is facing client specific issues leading to lower revenue growth in Q2FY25. “We had a very significant presence, and the client had a more abrupt scope reduction, leading into our revenue decline.” And lastly telecom which witnessed revenue decline in double-digits in September Quarter 2024. The telecom vertical is expected to recover only after the interest rate environment improves considerably, motivating companies to push for capex.

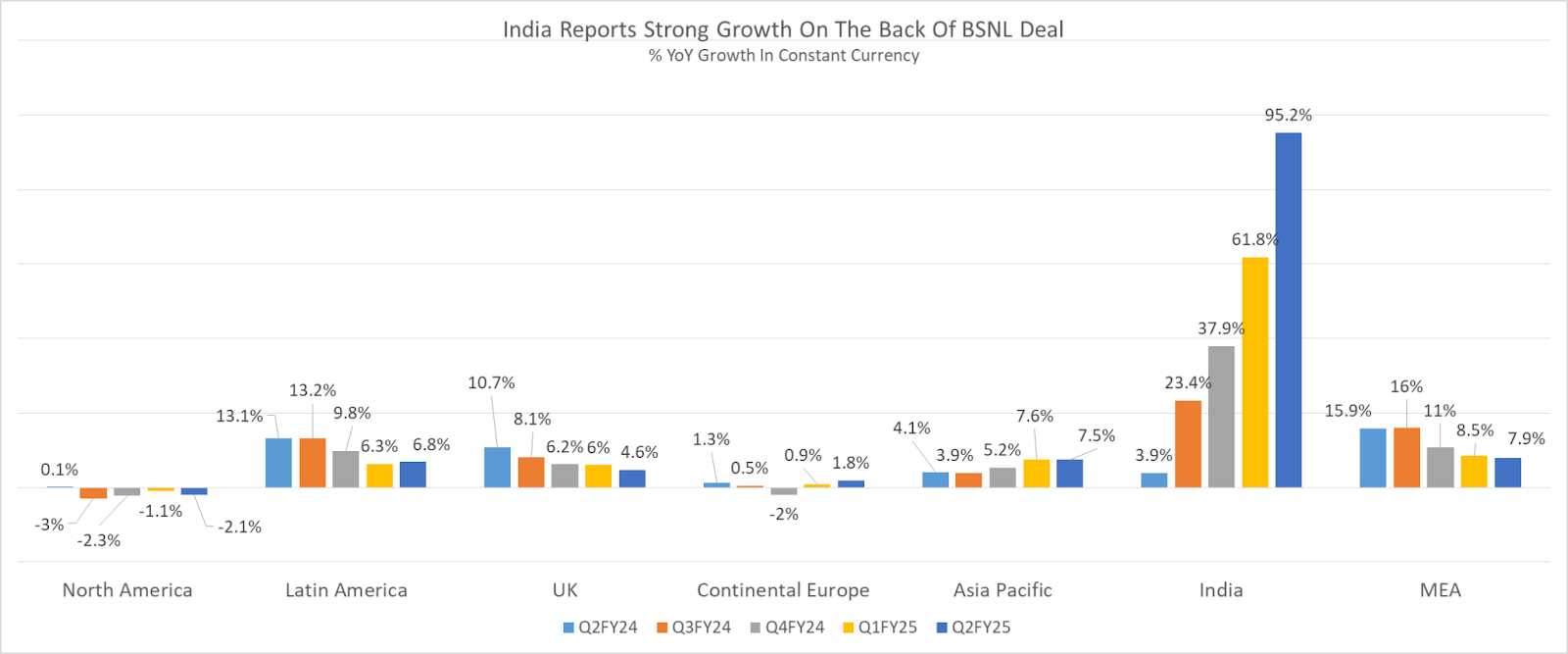

North America Continues To Report Negative Growth, BSNL Deal To End in 2025

In geographic revenue mix, except North America, all geographies performed well. North America revenue growth was dragged by the life sciences and healthcare segment which witnessed client specific challenges.

UK growth was also impacted by the healthcare vertical in September Quarter 2024. Highest growth was witnessed by India on account of the BSNL deal. TCS is rolling out 4G & 5G telecom infrastructure across India for BSNL. The deal is expected to be completed in 2025. According to the management, the BSNL deal is currently running at its peak and will report similar revenue growth for another quarter. By Q4FY25, revenue growth is expected to taper down. India revenue share in the overall revenue basket is 7.5%. Investors are more concerned about North American market revival. On this front, Krithivasan said that as uncertainties recede, growth will return. He further added that, “We believe the short-term freeze or cut down in the discretionary spend comes out as a market uncertainty. One that eases the investment should return, but I don’t want to say that it will immediately happen in Q3, but we believe in the medium term, it should happen.”