Indiastockguru Team

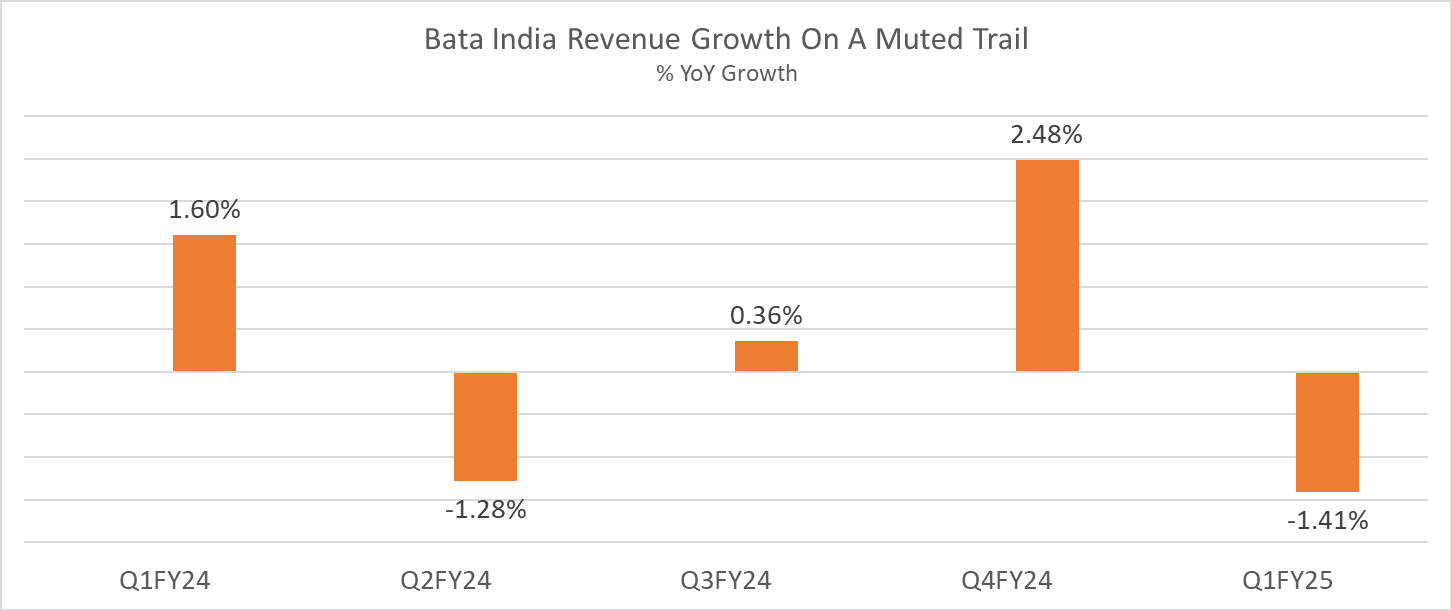

This is the fifth in a row for Bata India. Muted performance yet again by the market leader in the organized footwear space in Q1FY25.

While the premium category is doing well for Bata India, its core value and mass footwear category still bears the brunt of muted demand leading to lower revenue growth. Premium category above Rs 2,000 contributes 25%, value segment of above Rs 1,000 contributes 60% and less than Rs 500 category is nearly 15% of total revenue mix. Till Bata India does not enlarge its premium footwear segment or take strong price hikes in the value segment, revenue growth will remain muted. The company is unable to increase prices due to strong competition from regional and local players and lower discretionary spend by consumers. Speaking on value segment growth, Gunjan Shah, Managing Director and Chief Executive Officer at Bata India said,”I think in absolute, it is still not turned around completely. But we are hopeful seeing some of the signs that we are seeing on the ground on that front, that in the coming quarters, we should see that turning around for us.”

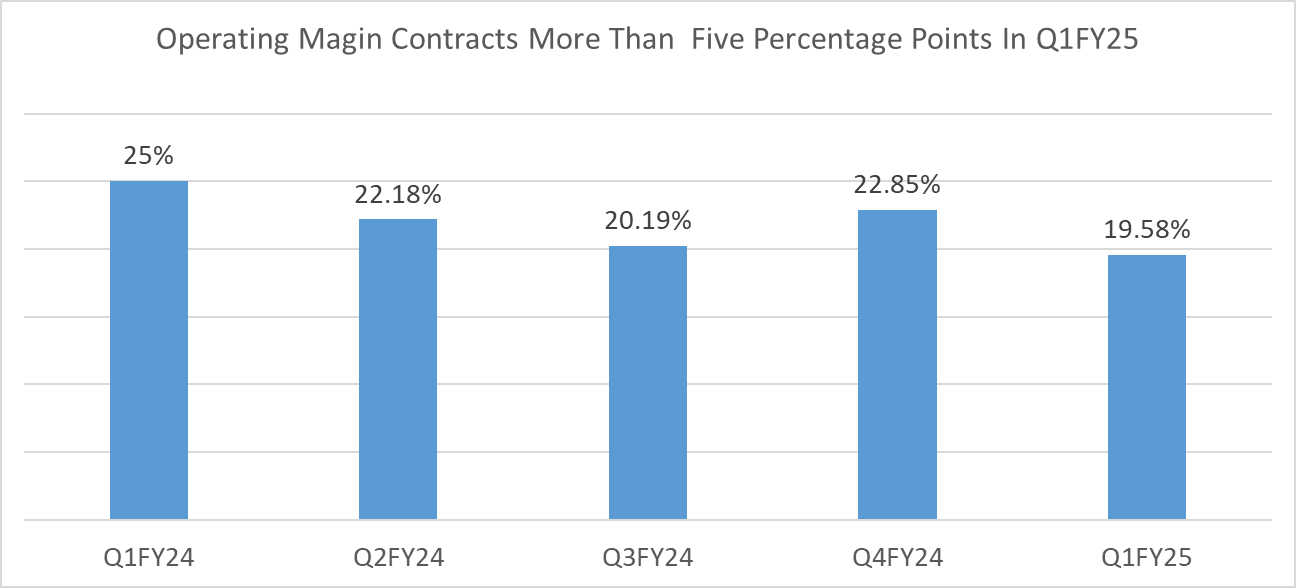

Revenues came in at Rs 945 crore, a fall of 1.4% YoY and operating margin at 19.6% contracted 542 basis points YoY in Q1FY25.

Bata India’s store network stands at 1916 as of June 2024 with 1350 company owned company operated (COCO) stores and 566 franchise stores. The management in its recent June Quarter 2024 result press conference said that 70% of its new store additions will be in tier III cities and below. While this will definitely increase penetration levels, what about the pricing strategy? Will the metro and tier I price levels be applicable in tier III and tier VI cities? Bata India prices its products 20% lower in tier II-VI cities compared to metro and tier I cities. In the short term, this pricing strategy presents growth challenges, in the long term this might pay off when growth returns. But when will growth return?