Indiastockguru Team

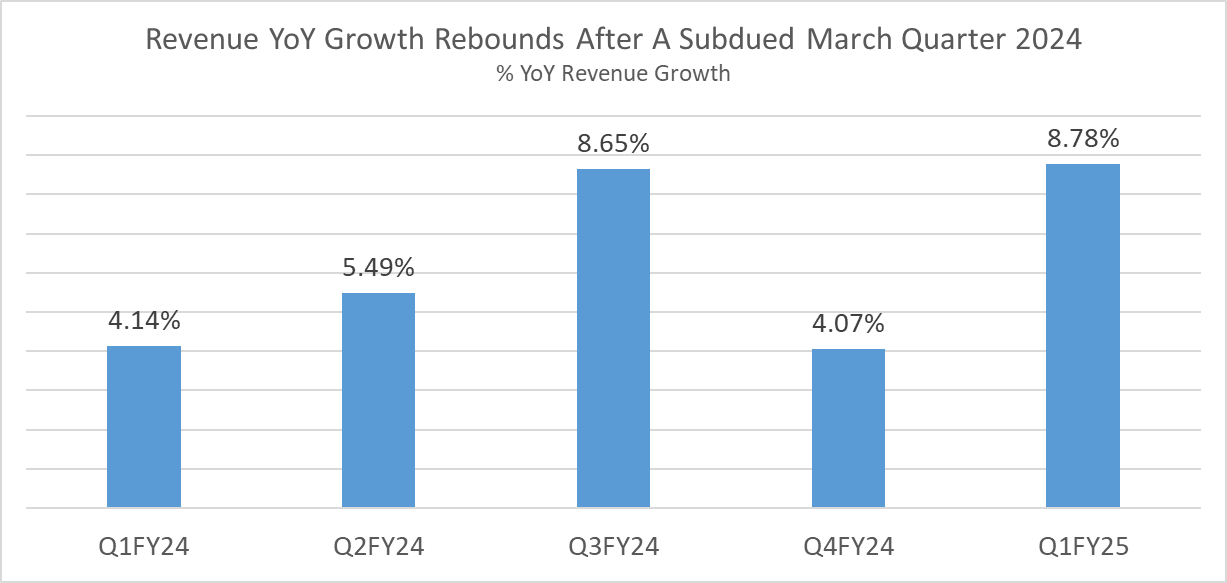

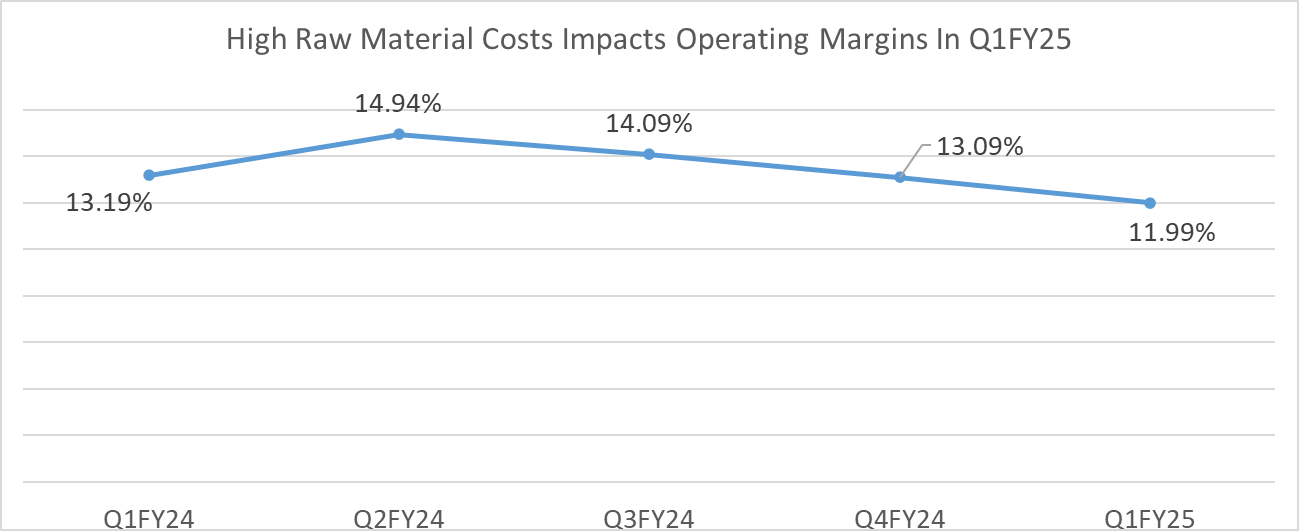

Ceat stock price fell 3% after June Quarter 2024 results were announced. The street was unhappy with 120 basis points (bps) margin contraction witnessed in Q1FY25 results. Revenue growth was stable at 8.8% YoY, highest over the past five quarters.

Revenues came in at Rs 3,193 crore in June Quarter 2024 compared to Rs 2,935 crore, same period previous year. Speaking on revenue growth, Kumar Subbiah, Chief Financial Officer at Ceat said, “The growth was driven by volumes and higher growth in more profitable segments like replacement and exports during the quarter.” Operating Margins came in at 11.99%, down 120 bps YoY due to high raw material costs in Q1FY25. Net profit stood at Rs 154 crore, up 6.6% YoY in June Quarter 2024.

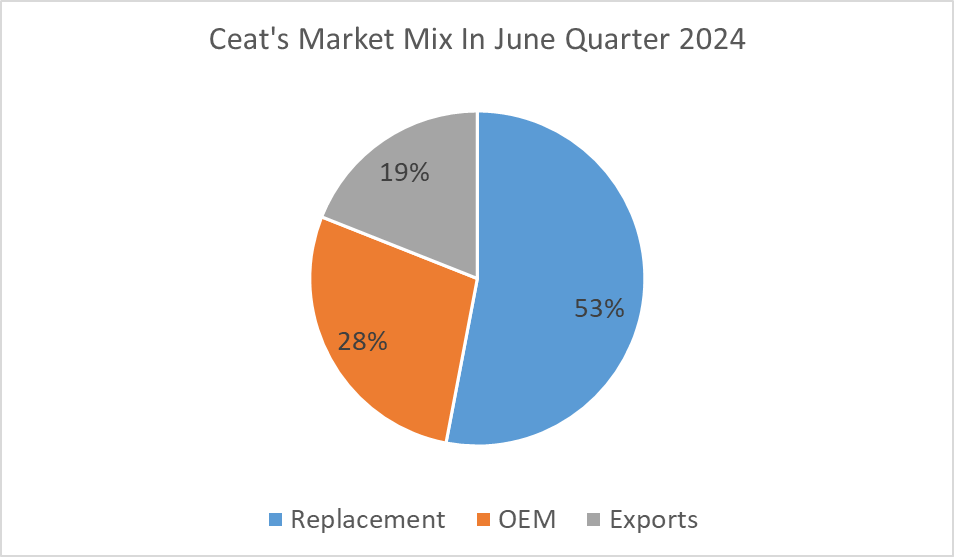

Replacement and Exports Drive Revenue Growth In June Quarter 2024

Ceat’s market mix is tilted in favour of the replacement segment followed by original equipment manufacturers (OEMs) and exports. The management aims to increase exports mix to 25% in the next 2-3 years.

Ceat reported volume growth of 8.7% YoY in June Quarter 2024. “Volume growth was led by replacement and international business with double-digit volume growth and a some-what muted growth in OEM segment.” According to the management, exports faced challenges such as non-availability of containers and significant freight hikes in Q1FY25. Latin America, Europe and the US are the major focus markets for Ceat. In the replacement segment, volume was led by commercial vehicles and the 2-wheeler categories. “Our saliency in premium categories is continuously up in the passenger segment as well as in the 2-wheeler segment”, said Arnab Banerjee, Managing Director and Chief Executive Officer at Ceat.

Raw Material Cost Impacts Margins, Rubber Prices At 13-year High

June Quarter 2024 witnessed exceptional rise in raw material cost. According to the management, higher raw material cost is singularly responsible for the contraction of margins in Q1FY25. Raw material cost is up 9% YoY in Q1FY25. While crude prices remained range bound during the quarter, rubber prices hurt margins with domestic rubber prices touching 13-year highs. Speaking on rubber prices, Banerjee said, “Domestic natural rubber prices have surged by about 25-30% over the past few months. And currently, it has scaled Rs 200 which is the highest in the last 13 years.” Presently, Indian rubber prices are at a premium to international rubber prices by Rs 10-12 per kg due to short-term supply demand gap. In addition to that, higher ocean freight has increased landed prices of imported rubber. While prices of natural rubber are expected to cool down, raw material prices are still expected to be above 5-6% QoQ, in Q2FY25. The management has put necessary controls on discretionary expenses and increased prices in various product categories to combat higher raw material costs.

Price Hikes Undertaken And Demand Outlook

To mitigate high raw material cost, the company has taken price hikes in the replacement segment in late May, June and July 2024. Price hike was close to 2.4% in the commercial segment, 2.5-2.8% in passenger segment and 1% in 2-3 wheeler segment. Speaking on OEM segment, Banerjee said, “In OEM, it is primarily indexed, we did not have too much of a price change in quarter 1. However, in quarter 2, we see an indexation benefit of already 2%.” He further added that the price hikes were back ended and most of it will flow through in quarter 2 in international business. Thus, price hike benefit is expected to improve revenue growth in September Quarter 2024. The management also expects good rural demand with strong pick up in monsoon activity in July-August period. Consequently, two-wheelers and farm tyres are expected to witness good demand. The management also expects good growth in the four wheeler segment supported by strong investment in highways by the government and longer number of travelling hours leading to stable demand. In the truck-bus radial (TBR) segment, Banerjee said, “Our growth in truck-bus radial has also been pretty robust, and we are 100% sold out from the Halol capacity. As our Chennai TBR capacity comes on stream by end of Q2FY25, we expect renewed growth in the truck-bus radial segment as well in replacement, mining, construction, all these areas are doing well.”