Suhani Adilabadkar

India Cements stock price touched its new 52-week high of Rs 372.85 on July 29, 2024. The stock price has gained 20% since the last week of June this year. UltraTech Cement, market leader in the domestic cement industry had acquired 22.77% stake in India Cements from ace investor and owner of DMart retail chain, Radhakishan Damani in June 2024.

On July 28, 2024, the Board of Directors of UltraTech approved the purchase of a 32.72% equity stake of the promoters & their associates in India Cements Limited. While the 22.77% stake on June 28, was purchased at a price of Rs 268 per share, the promoter group equity is acquired at Rs 390 per share. This will trigger a mandatory open offer. As per the UltraTech press release, an open offer at Rs 390 per share will be done subsequently after obtaining all regulatory approvals.

South India, A Battleground for UltraTech Cement And Ambuja Cement

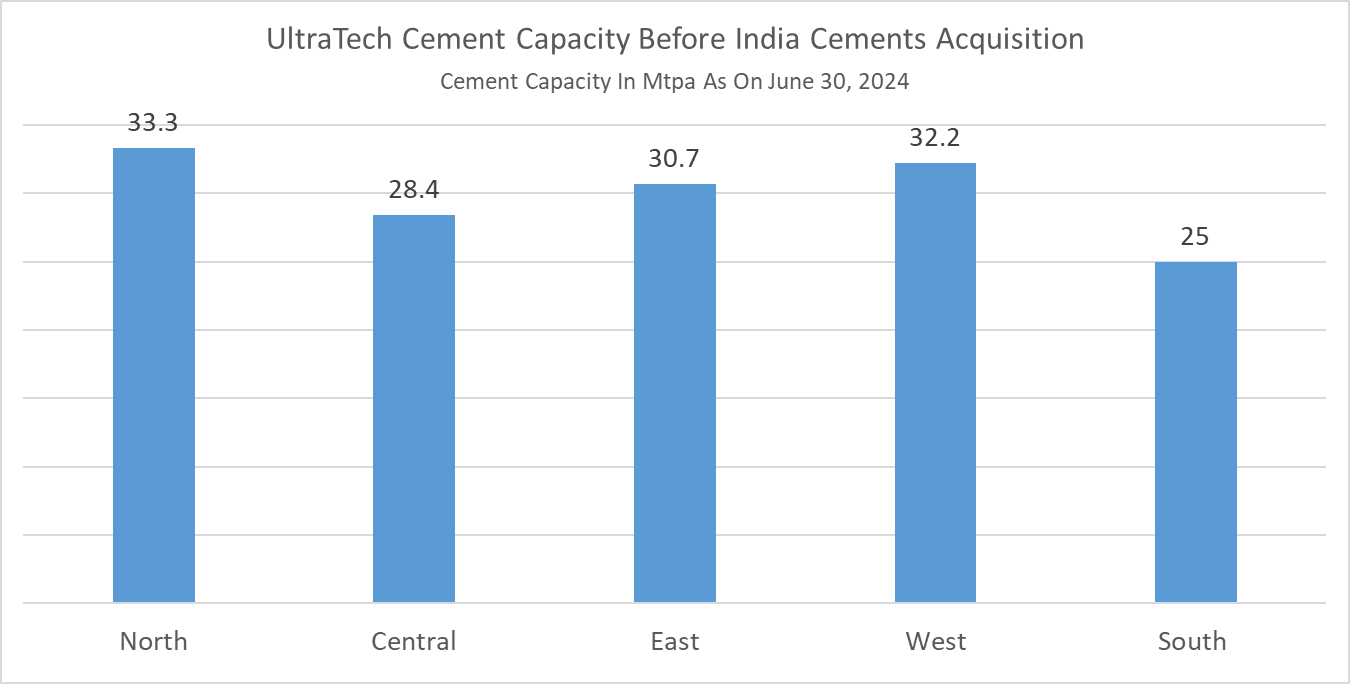

UltraTech Cement is the cement flagship company of the Aditya Birla Group. The company is the third largest cement producer in the world, outside of China, with a total domestic cement capacity of 149.5 million tonnes per annum (Mtpa) and 5.4 Mtpa overseas as on June 2024. The company is undertaking both greenfield and brownfield aggressive expansion across India to increase its capacity which is expected to be around 157 Mtpa by FY25. This expansion excludes acquisition of Kesoram Cement (in November 2023) with a capacity of 10.75 Mtpa awaiting regulatory approvals. UltraTech further aims to achieve cement capacity of 183.5 Mtpa by FY27. The company reported revenues of Rs 18,070 crore, a rise of 2% YoY in June Quarter 2024. Net profit came in at Rs 1,697 crore in Q1FY25.

Cement industry took a turn with the acquisition of Holcim stake in Ambuja and ACC by Adani Group in September 2022. Adani Group has consolidated its cement business under Ambuja Cement, currently the second largest cement manufacturer in India. And both players, Ultratech and Ambuja Cement are focussing on southern India’s fragmented cement market with more than 40 small players ideal for market share consolidation. After acquiring Sanghi Industries last year and its latest acquisition, Penna Cement in June 2024, Ambuja Cement’s capacity now stands at 89 Mtpa. The company aims to increase its cement capacity to 140 Mtpa by 2028. With aggressive peers like Adani in the backdrop, UltraTech Cement owned by Kumar Mangalam Birla cannot play the passive game in the domestic cement industry. India Cements acquisition will add 12.95 Mtpa capacity in southern India, where Ultratech Cement has low cement capacity. India Cements total capacity is 14.45 Mtpa, of which 12.95 Mtpa capacity is in the South (particularly Tamil Nadu) and 1.5 Mtpa is in Rajasthan. Thus, UltraTech Cement capacity in south India cement will be 37.95 after the India Cements acquisition is completed.

Large Companies Play Price War Games, Smaller Manufacturers Suffer

High cement prices during the pandemic were driven by increased input costs, Russia-Ukraine war and strong infrastructure push by the central government. Cement prices have cooled down considerably in 2024 from a high of Rs 400 per bag, in 2022. In fact, cement prices have been on a downward trend since November 2023. Cement prices are currently at Rs 370 per bag. Higher competitive intensity has also pushed prices lower as manufacturers focus on expanding capacities to gather market share and sell more volumes. Larger scale and capacity leads to higher operational efficiency, lower cost of production and cement companies are able to maintain profitability amid lower cement prices. Cement manufacturers are also investing in green energy through solar plants and waste heat recovery systems (WHRS) to reduce their cost of power consumption and navigate lower cement prices. Speaking on WHRS, Atul Daga, Chief Financial Officer at UltraTech Cement said, “The average cost of WHRS power would be almost Rs 0.85-0.90 per unit compared to our average cost of power around Rs 7 per unit.” Thus, large players can maintain their operating margins and bottom-line through considerable cost savings and keep cement prices lower, hurting small players. The demise of India Cements is the best example of the price wars and gradual building up of cement oligopoly in India.

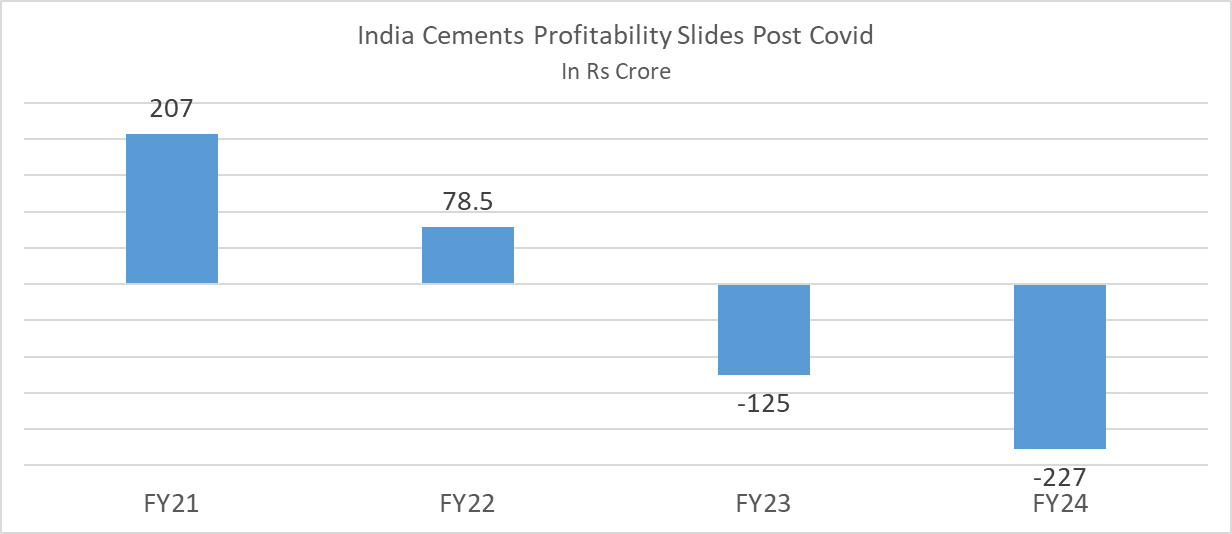

India Cements Financial Stress Led To Its Demise

India Cements acquisition was initiated by Radha Krishan Damani’s stake sale to UltraTech Cement. With 22.77% stake already in its pocket, it was easier for the market leader to negotiate and acquire India Cement’s promoter group stake. Out of the 32.72% promoter group stake, 28.42% belongs to N Srinivasan. And of this, 47.4% stake is pledged. India Cements has been reporting annual losses for the past two years.

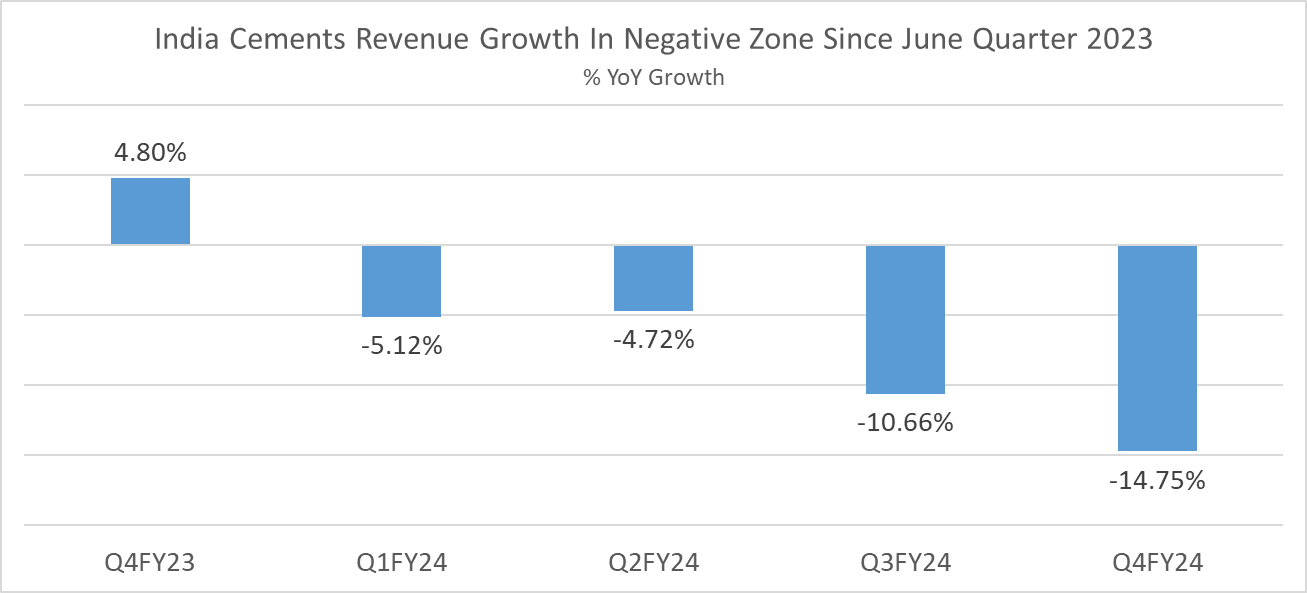

Revenue and operating profit CAGR for the past 5 years stands at -2.4% and -31% respectively. In quarterly terms, revenue YoY growth has been in negative territory over the past four quarters.

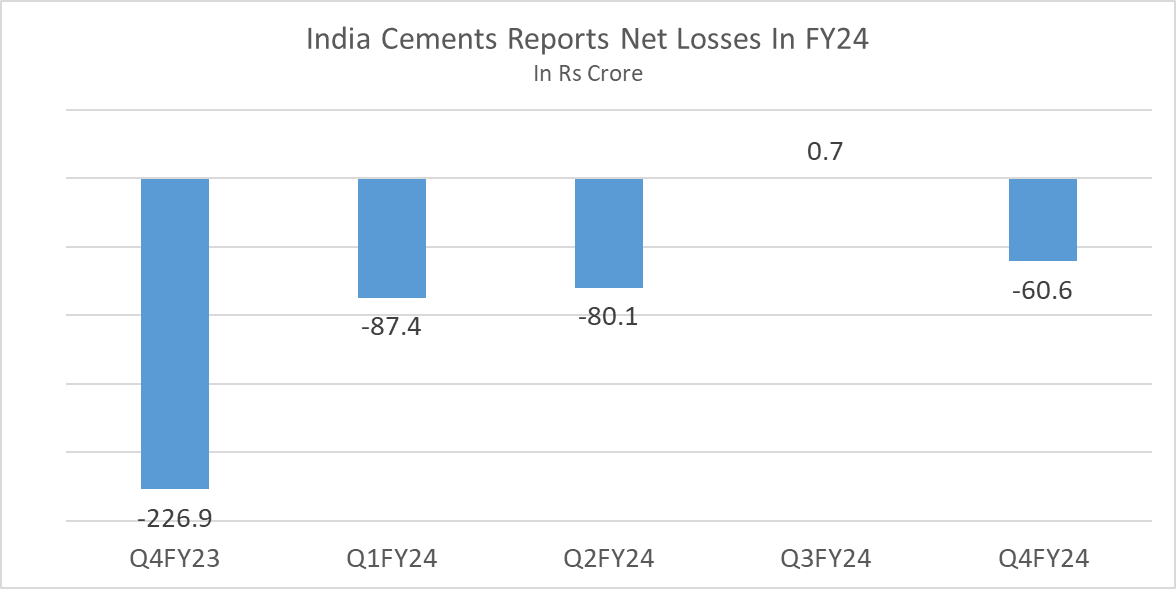

India Cements reported revenues of Rs 1,267 crore, a fall of 14.75% YoY in March Quarter 2024. Operating profit of just Rs 38 crore and net loss of Rs 60 crore was reported in Q4FY24.

Post Covid, the Indian cement sector is in a consolidation phase. Large companies with deep pockets are looking to buy out smaller players to increase their pan India presence. Small regional players under financial duress should be vigilant.