Suhani Adilabadkar

Tata Consultancy Services (TCS) stock price soared 7% on June 12, 2024 driven by better-than-expected June Quarter 2024 results, announced a day before after-market hours. The IT bell-weather’s resilience continued into FY25 with strongest constant currency (cc) YoY growth over the past four quarters, robust operating margins and positive momentum witnessed in the banking, financial services & insurance (BFSI) segment. Amid a challenging environment, TCS reported a commendable performance in Q1FY25. But with the overall global situation still being volatile, the TCS management maintained its cautious outlook for FY25.

Resilient June Quarter 2024, Operating Margins Fall QoQ

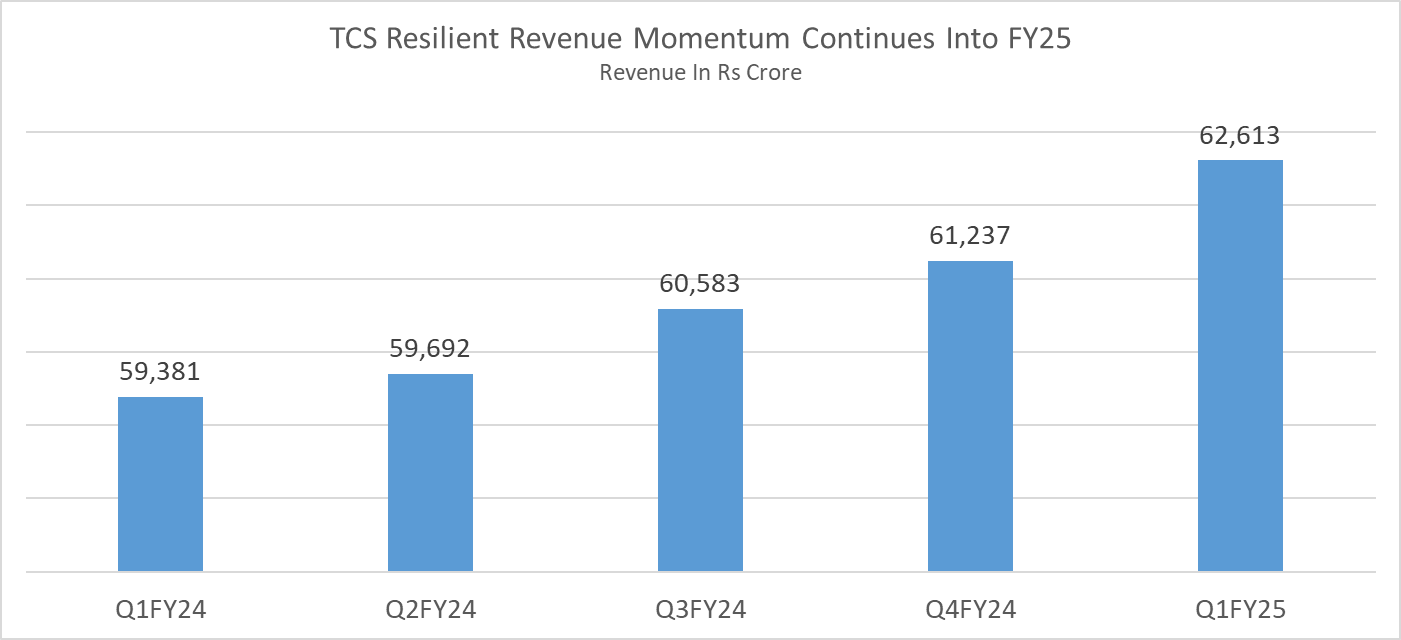

TCS reported revenues of Rs 62,613 crore, up 5.4% YoY supported by UK and India markets in Q1FY25.

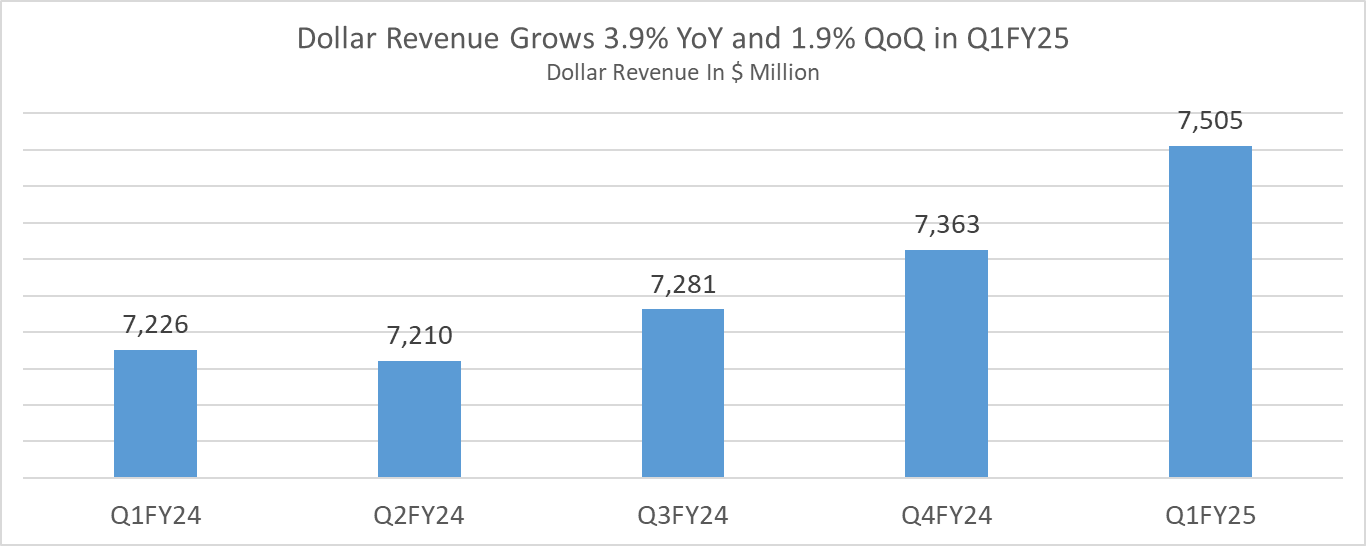

Dollar revenues grew 3.9% YoY to $ 7,505 million in June Quarter 2024 compared to $ 7,226 million, corresponding quarter previous year.

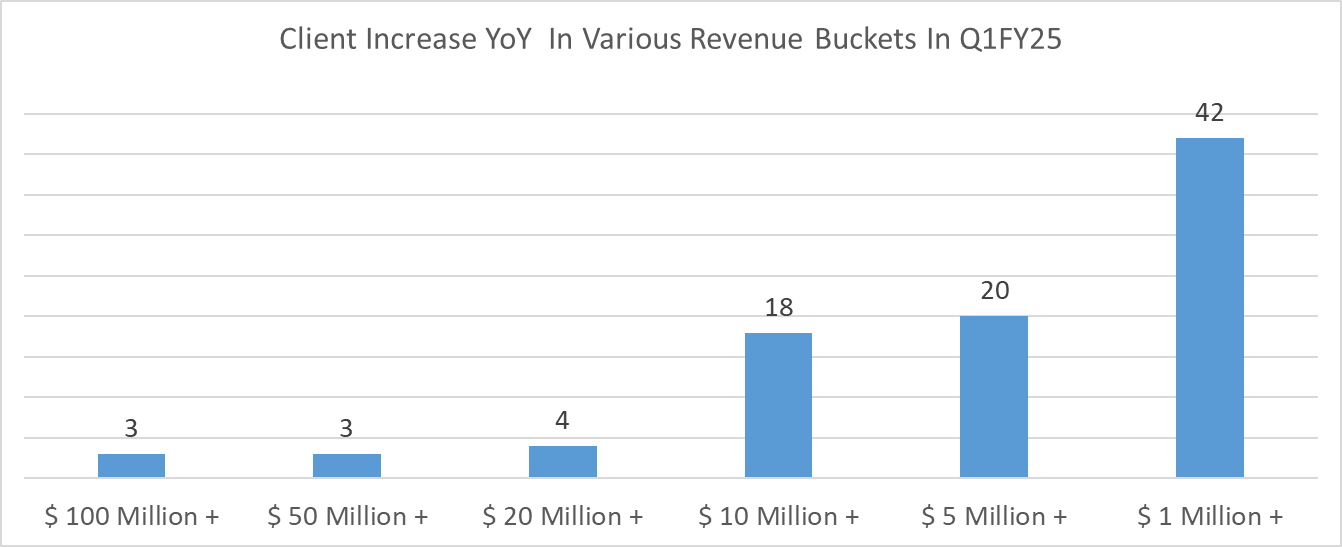

Constant currency revenue growth stood at 4.4% YoY in Q1FY25. The company added three clients each in the $ 100 million and $ 50 million revenue bucket in June Quarter 2024.

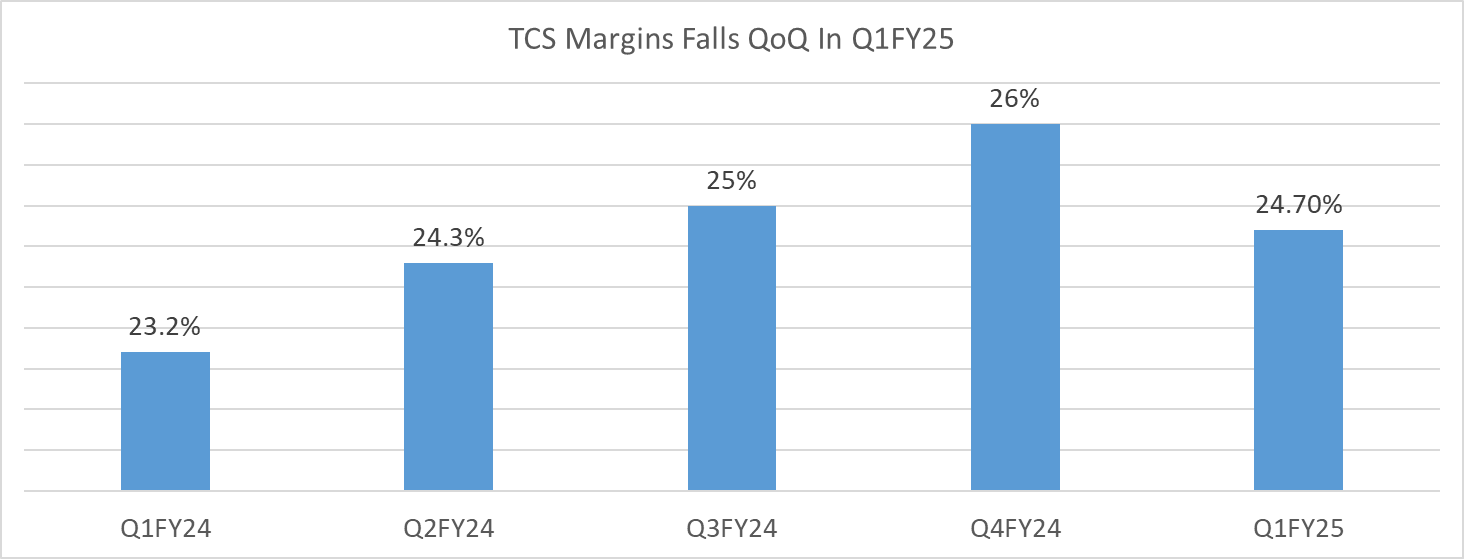

Operating margins at 24.7% expanded 150 basis points (bps) YoY supported by operating efficiency, improved utilization and reduction in subcontractor expenses. Operating margins expanded despite a 170 bps headwind from annual wage hikes undertaken in April 2024. Consequently, QoQ operating margin fell 130 bps in Q1FY25. Net profit stood at Rs 12,040 in June Quarter 2025 compared to Rs 11,074 crore, same period previous year.

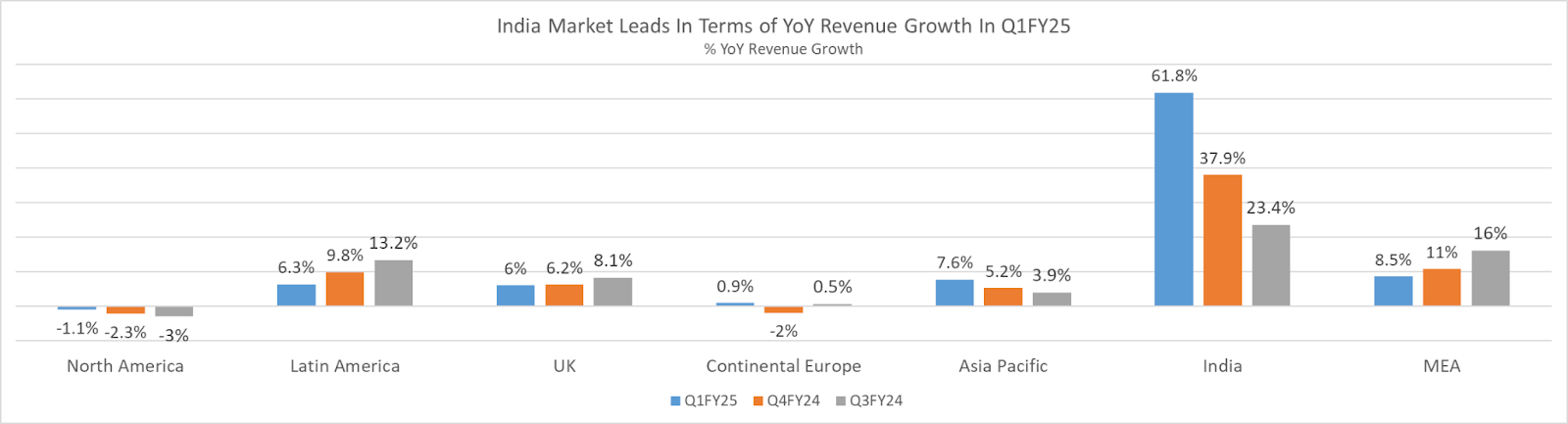

Growth Led By India, North America Improves In Q1FY25

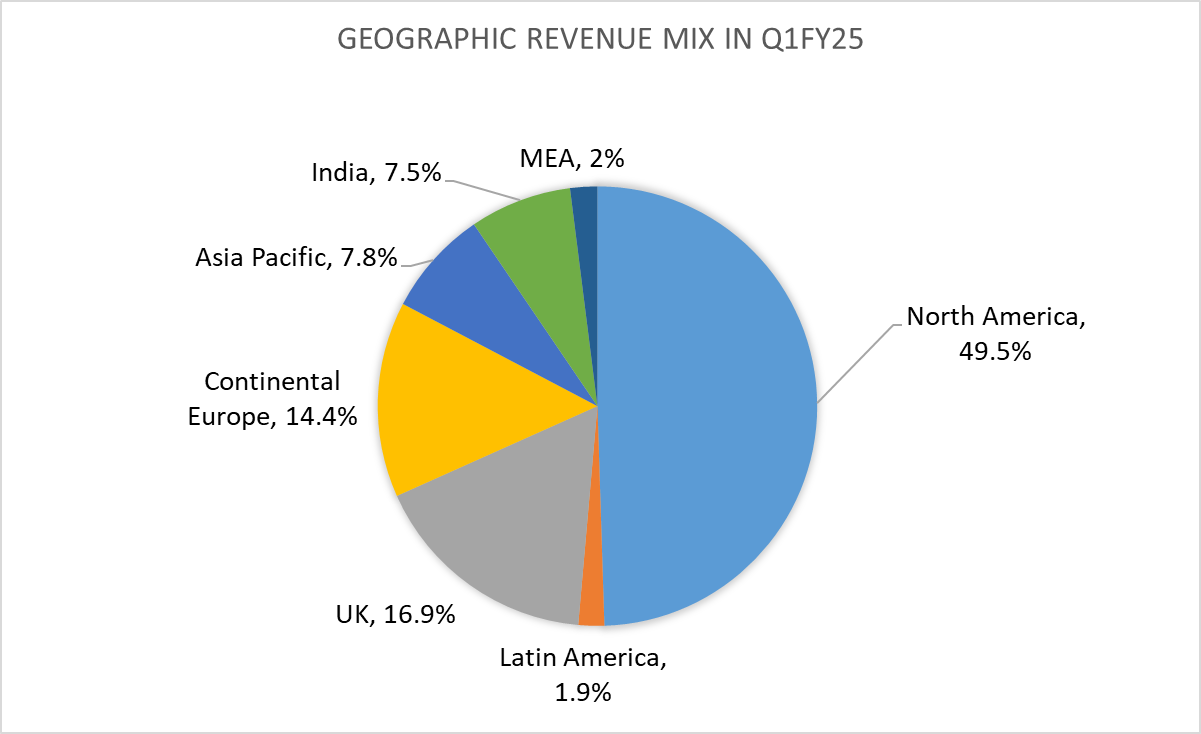

TCS June Quarter 2024 witnessed broad-based growth across all geographies and its major business verticals. India revenue growth of 62% YoY was driven by the BSNL deal. TCS is rolling out 4G & 5G telecom infrastructure across India for BSNL. The deal is expected to be completed in 2025. While India’s share in the overall revenue basket is 7.5%, TCS also performed well in its largest market, North America with a sequential growth (up 0.9%) after five quarters. Speaking on the North American market, K Krithivasan, Chief Executive Officer and Managing Director at TCS said, “Overall IT services spending is stable, however, clients are neither going for large scale capex initiatives nor ramping down with deep spending cuts.”

While North America reported revenue de-growth of 1.1% YoY in Q1FY25, the largest revenue contributor with 50% revenue share has improved from a 3% YoY revenue decline witnessed in December Quarter 2023. In the next major market, the United Kingdom, IT services spend continues to be more resilient leading to 6% YoY revenue growth. While European revenue growth was flat, Latin America, Asia Pacific and MEA markets were stable reporting 6.3%, 7.6% and 8.5% YoY growth respectively in June Quarter 2024.

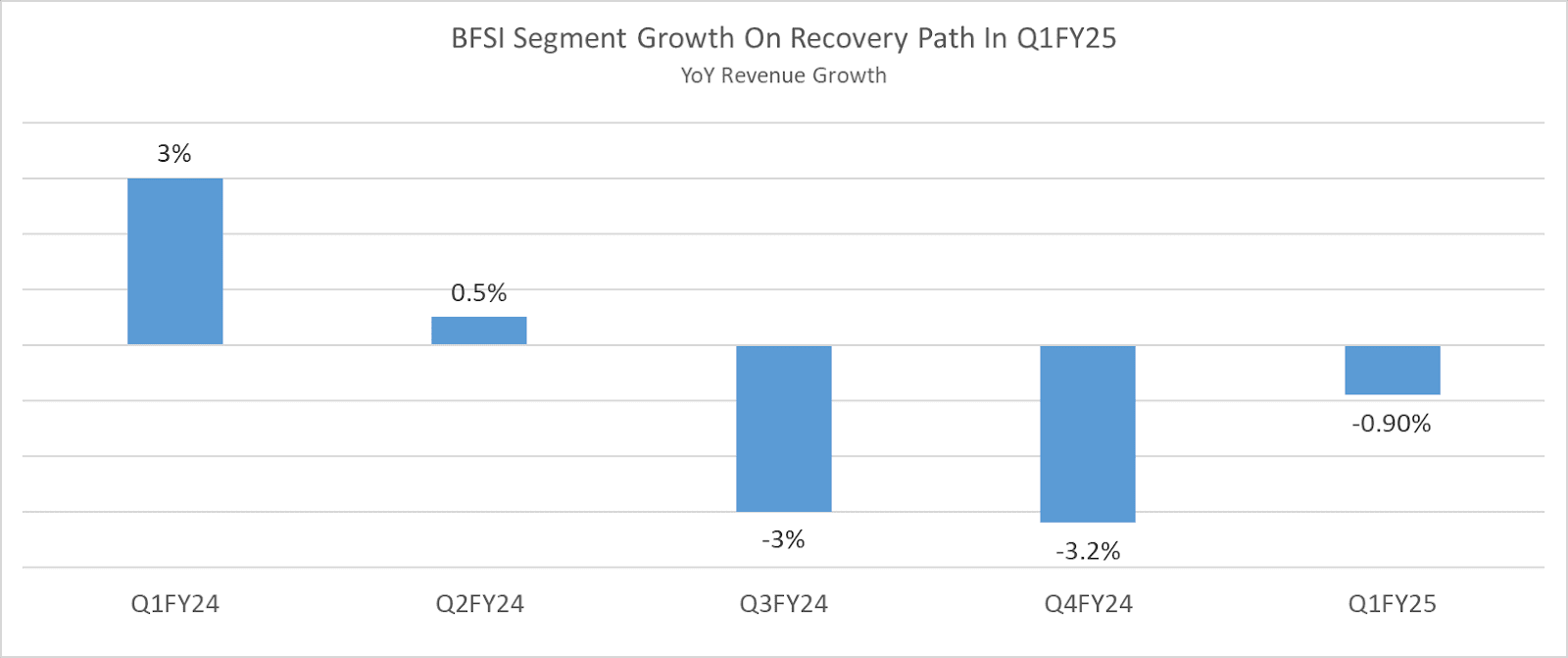

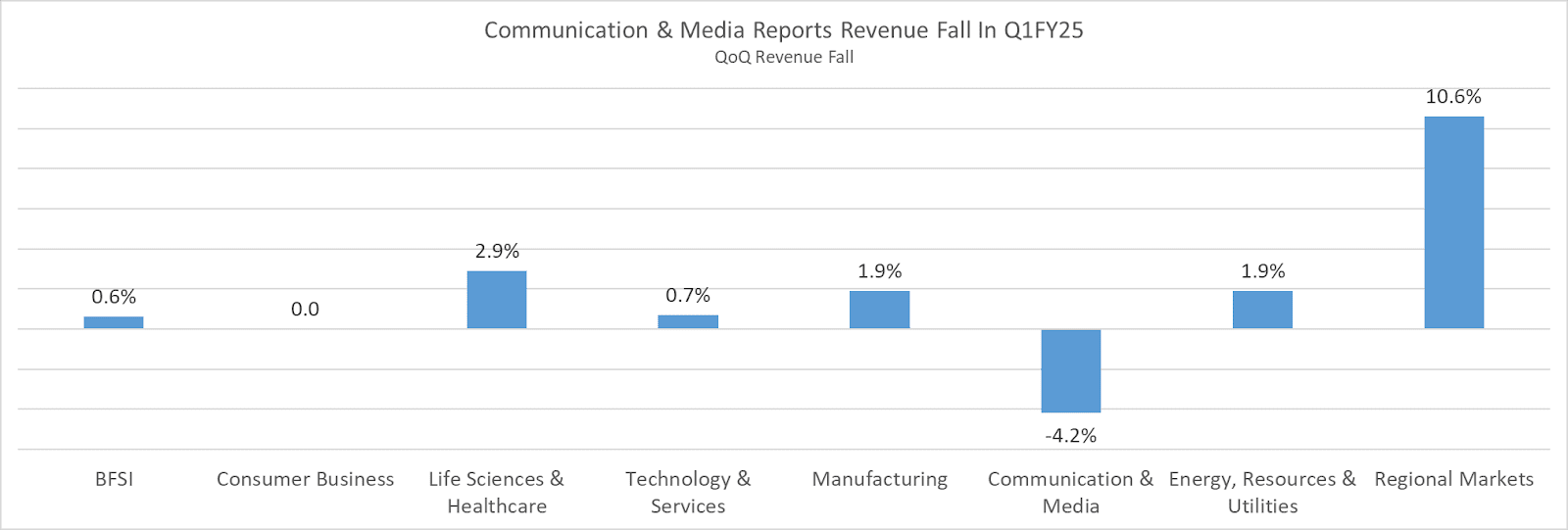

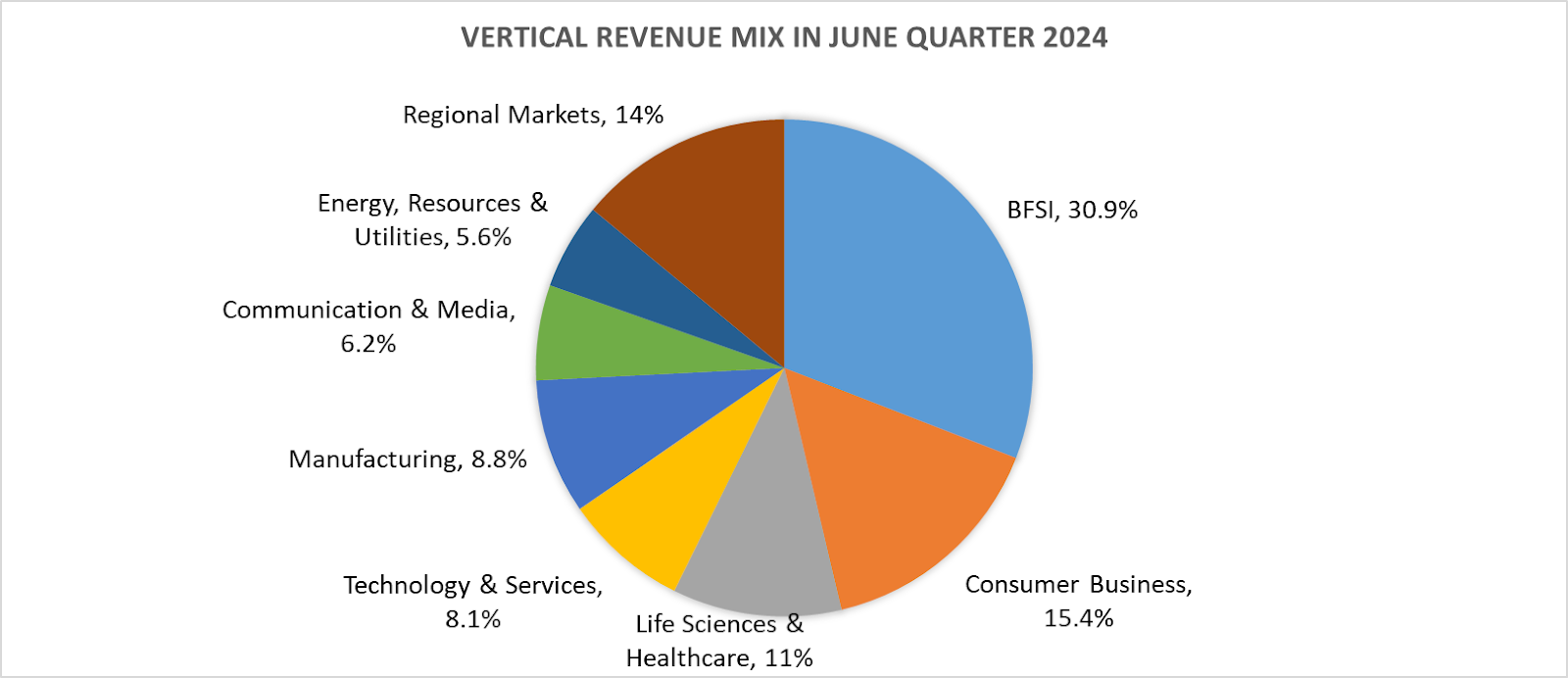

BFSI On Recovery Mode, Communication & Media Still In Negative Territory

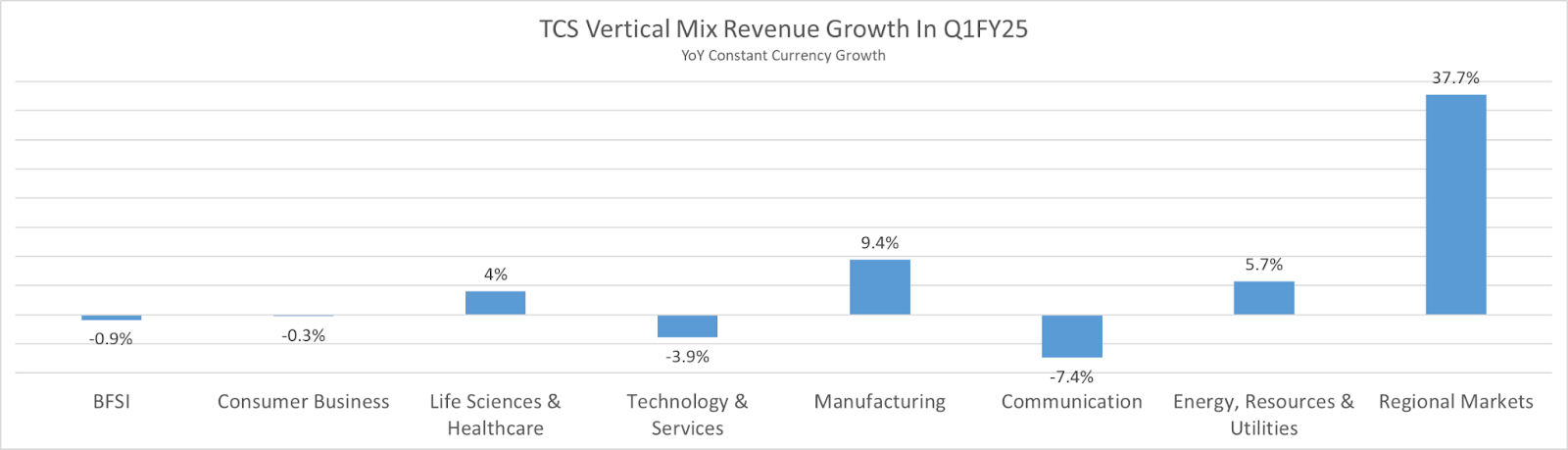

Banking Financial Services and Insurance (BFSI) contributed nearly 30% to TCS revenue basket in Q1FY25. After reporting strong double-digit growth throughout FY23, BFSI YoY growth rates have slumped in FY24. BFSI vertical revenue growth stood at 0.6% sequentially and -0.9% YoY.

Speaking on BFSI, Krithivasan said, “For the BFSI industry, the wave of the net interest income that was strong in 2023 has been waning down in 2024. Clients are now balancing their transformation priorities to ensure business resilience and innovation to improve cost to income ratio.” He further added that “BFSI performance to a great extent is, I would say, North America performance as well.” Thus, for BFSI to go back to double-digits, technology spending revival in the US market is needed which can be spurred by lower interest rates. Clients in the BFSI segment are more focused on cost optimization deals with immediate return on investment (ROI) than discretionary projects with lower ROI.

Not only BFSI, retail and communication verticals are also awaiting loosening of interest rates. In the consumer business or retail segment, clients are prioritizing cost optimization projects with higher ROI over discretionary spend. In the retail sector too, a lot depends on the interest rates movement and consumer confidence for clients to loosen their purse strings. Retail vertical reported -0.3% revenue de-growth YoY in June Quarter 2024. Communication & Media vertical continues to face business challenges and declined 7.4% YoY in revenue terms in June quarter 2024. Telecom companies had invested heavily during the pandemic for 5G rollout but have not achieved the expected return so far. For them to embark on investment, a lower interest rate environment would be a favourable trigger factor. All business verticals have reported positive sequential growth in Q1FY25 except communication & media.

Manufacturing vertical continued its strong performance reporting 9.4% YoY revenue growth driven by smart manufacturing, renewable energy, battery energy storage systems (BESS) and grid modernization. According to the management, the automotive industry is being reshaped by the advent of electric vehicles which might change the investment priority of clients in the near future.

Another vertical that reported YoY revenue de-growth was Technology and Services at -3.9% but returned to sequential growth after 5 quarters in Q1FY25. Customers in this vertical remain cautious about new spending until business growth momentum picks up. And lastly Energy Resources and Utilities, the smallest vertical with just 5.6% revenue share grew 5.7% YoY in June Quarter 2024 driven by renewables generation capacity and transmission & distribution projects.

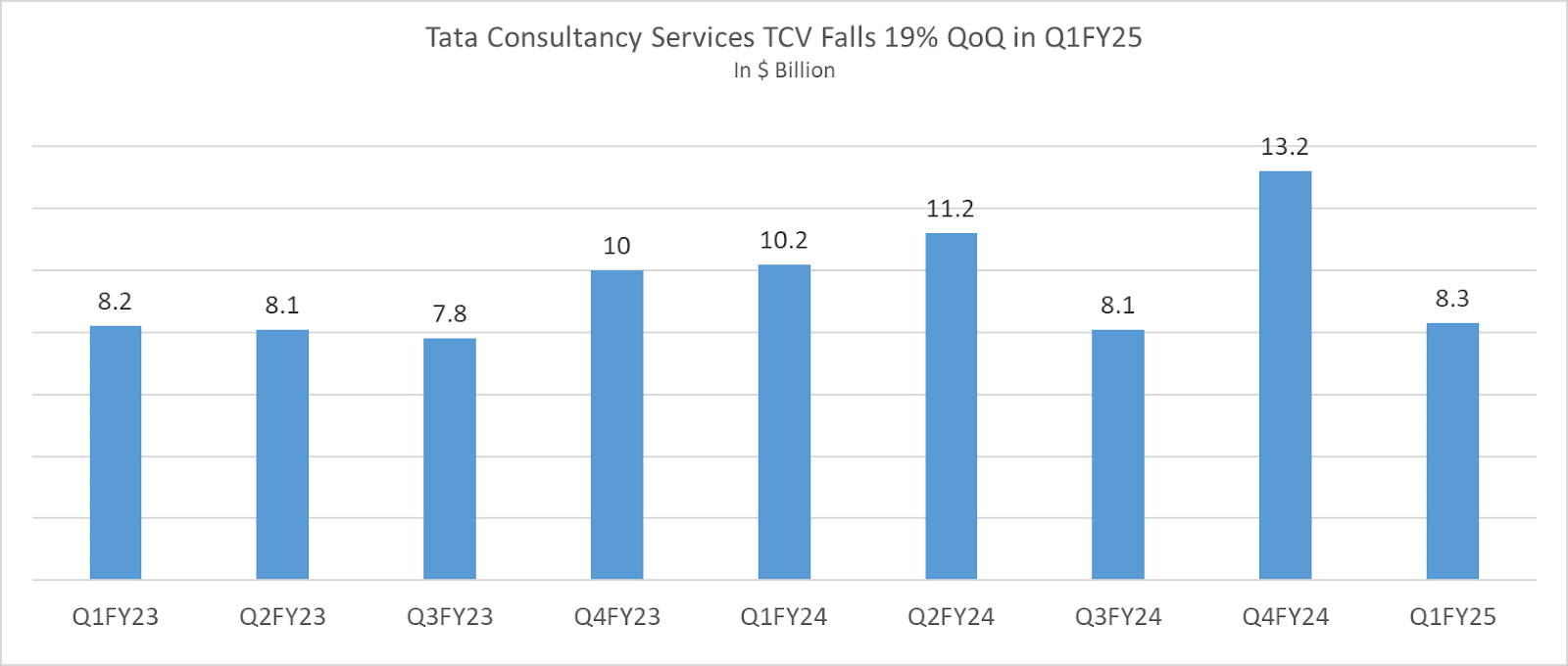

Early To Call Out Growth Stability, TCV In Comfort Zone

Demand visibility has improved since December Quarter 2023. But, even with better-than-expected results in Q1FY25, the TCS management is not calling out sustainability of these numbers in the coming quarters. While the management is confident that FY25 will be better than FY24, uncertainty still persists. “We still see situations where clients are ramping down programs or re-evaluating programs at very short notice. And that is the reason we believe that it is too early to call a sustained growth momentum or a demand stability”, said Krithivasan. While the TCS management has stopped giving guidance in terms of revenue growth, total contract value (TCV) or order indicates growth potential in the near future. TCV in Q1FY25 stands at $8.3 billion.

The TCV has been lower in June Quarter 2024 compared to previous March quarter 2024. TCV has fallen 19% sequentially and 37% YoY in Q1FY25. Speaking on lower TCV, Krithivasan said, “Some of the large programs that we thought that we would close were pushed back by a few weeks or maybe a month or so. But we’re confident those orders will be booked in Q2FY25.”

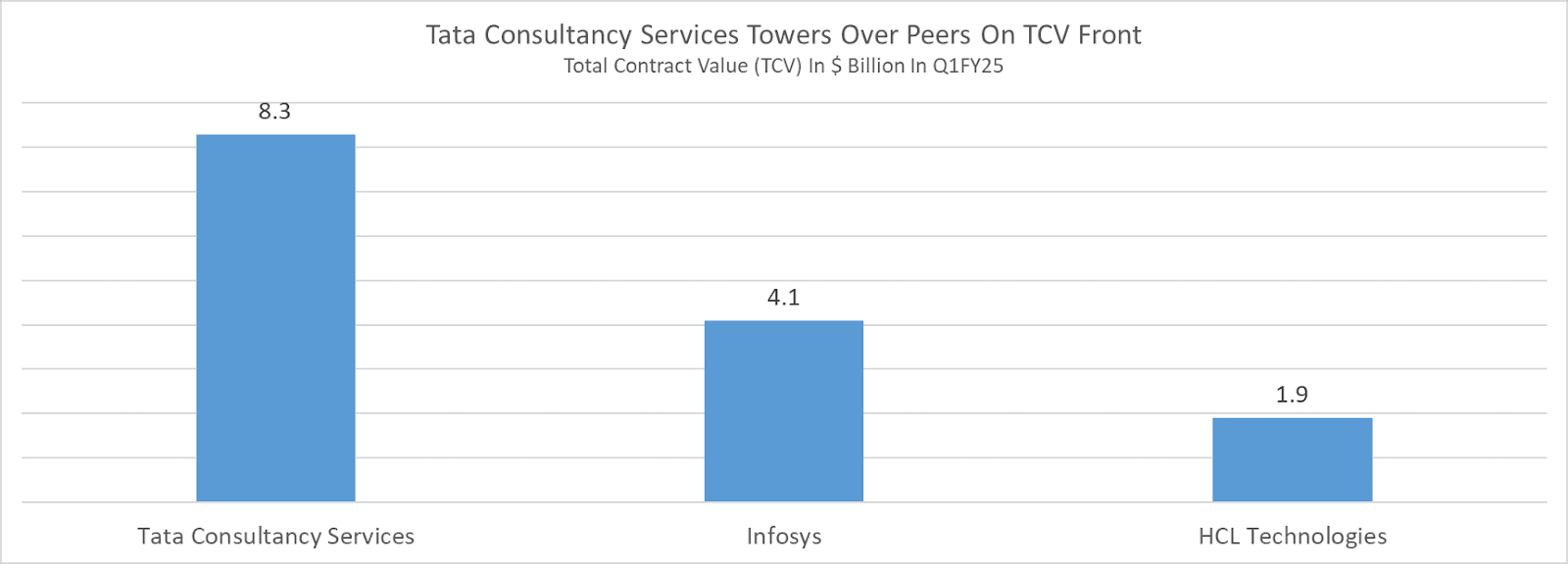

According to the management, the June Quarter TCV is within their $7-9 billion per quarter comfort zone. Tata Consultancy Services BFSI TCV stands at $2.7 billion and North America TCV in Q1FY25 was $4.6 billion, higher than total order book or TCV of Infosys.