Bata India stock price is near its 52-week low. The company delivered yet another muted quarterly performance on February 1st, 2024. Revenue growth was flat, operating margins fell three percentage points YoY and net profit declined 30% YoY in December Quarter 2023. Bata stock price has lost 5% since its Q3FY24 result announcement.

December Quarter 2023 – Not surprisingly Bata

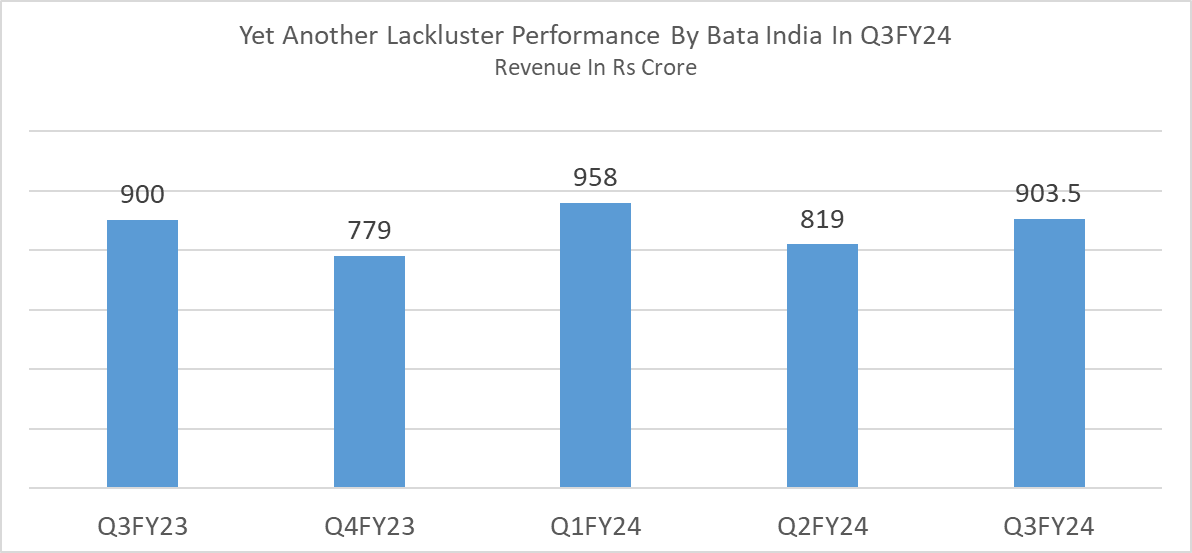

December Quarter 2023 is the third successive quarter of muted revenue growth and negative net profit YoY growth for Bata India. Revenue from operations came in at Rs 903 crore with 0.36% YoY growth in Q3FY24 due to weak demand mainly in the mass market footwear segment. Mass market segment constitutes nearly 40-50% of the overall Bata revenue mix. According to the management, while the mass market segment witnessed sluggish demand, the premium category performed well.

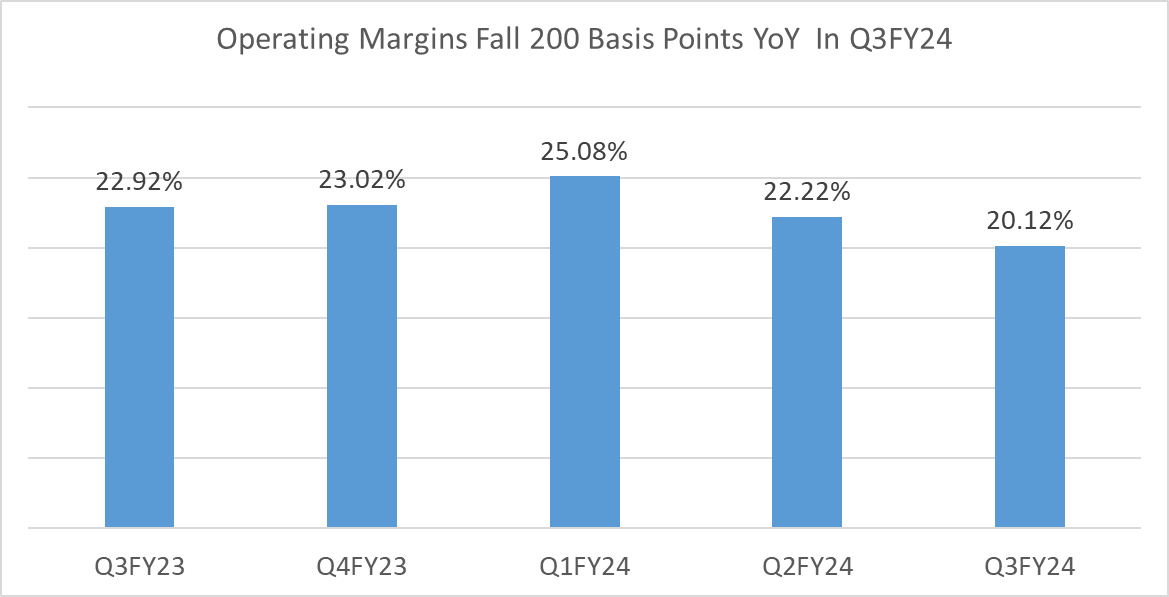

Operating margins came in at 20% in Q3FY24 compared to 22.9% in the same period corresponding quarter, a 290 basis point contraction YoY. Operating margins fell due to higher advertisement spends and ERP implementation cost in December Quarter 2023. Net profit stood at Rs 58 crore in December Quarter 2023 against Rs 83 crore, same period previous year, a fall of 30% YoY.

On a muted growth trail, Bata India on the backfoot

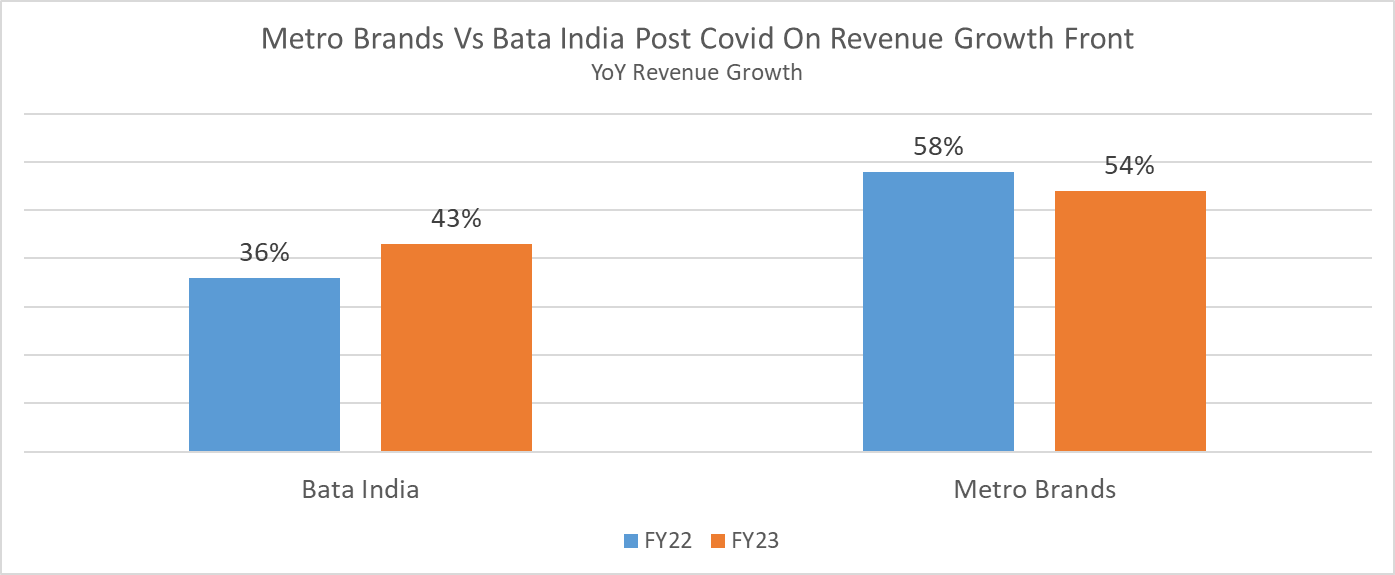

Bata India reported revenue growth of 36% and 43% YoY in FY22 and FY23 respectively. While FY22 revenue growth was on a negative base of -42% in FY21, revenue numbers in FY23 were supported by the post Covid spending boom. Close peer, Metro Brands annual revenue YoY growth numbers in FY22 & FY23 were even better.

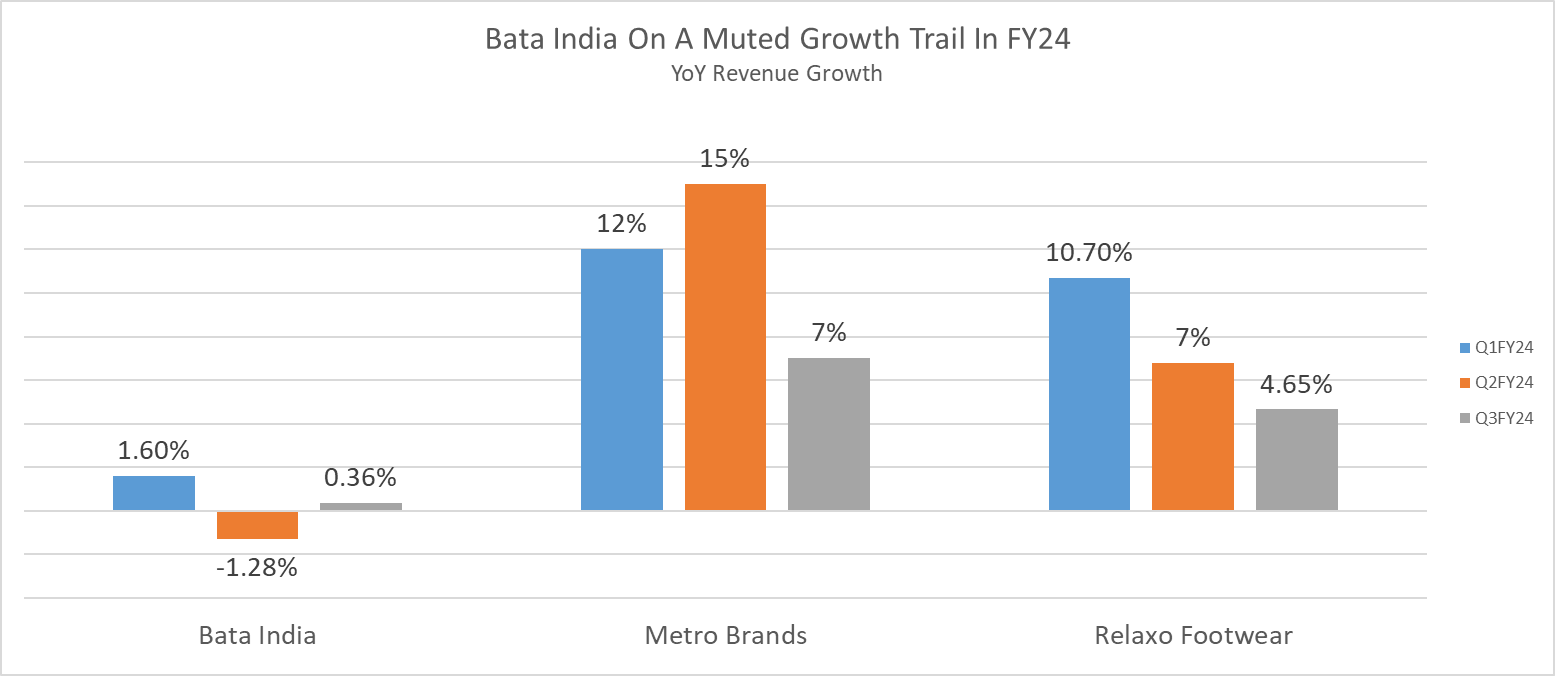

Fast forward to 2023-24, the past three quarters have been muted both in terms of revenue and profitability. While the Bata management blames weak demand for lower revenue and volume growth in December Quarter 2023, Metro Brands has a different reason. According to Metro Brands management, headwinds from Covid bump last year and inflated inventory which led to aggressive clearance sales by many footwear retailers impacted growth in Q3FY24. Though slowdown in discretionary expenditure is definitely seen in the footwear industry, Metro Brands and even mass market leader, Relaxo Footwear performed better compared to Bata India in FY24.

Is the premiumization story doing well?

While the management has been gung-ho about its premiumization story, it has not translated into strong volume growth. Bata reported mid-single digit YoY volume growth in Q3FY24 on a base of -5% YoY volume growth in December Quarter 2022. Speaking on the premium category, Gunjan Shah, Managing Director and Chief Executive Officer at Bata India said, “The premiumisation journey continues. Premium categories did outgrow our overall portfolio growth driven by Floatz, [Comfit], basically the Hush Puppies and the Bata Comfit brand.” If the premium category (which also includes sneaker brands) is doing so well quarter after quarter, then why has there been no price increases even in the premium category for the past six quarters. “For almost six quarters, we have stopped price increases so it’s largely the premiumization that is driving ASP increase and we are hoping that the stability of pricing will eventually help us turn around the mass market demand perspective from consumers”, said Shah. The company reported mid-single digit average selling price (ASP) expansion in Q3FY24. But will the mass market segment revive for Bata India. The company is waiting for inflation to completely come in control and income levels to improve. Haven’t the consumer’s tastes, trends, style and attitude changed post-Covid. With the unorganized segment coming strongly post Covid and online footwear retailers finding a way with Gen Z, impacted Bata’s mass market segment. Flatheads, Funkfeats, Cozywalks, Cai Store are some of the popular footwear online retailers.

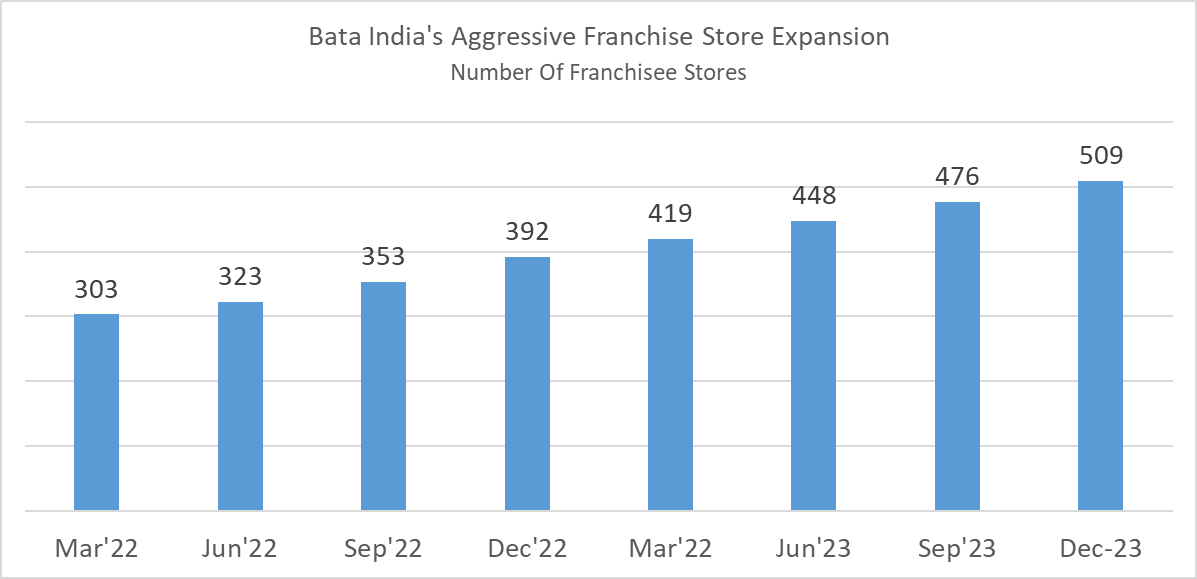

Franchise expansion continues, volume and revenue growth remains muted

Bata India is expanding aggressively through its franchise stores in tier 2-4 cities now touching 500 numbers in December 2023, but revenue growth is still muted. This is simply because ASP is 20% lower in tier 2-4 cities compared to metro cities. The company total store count stands at 1835 stores with 1326 company owned company operated (COCO) stores as on December 2023.

Thus, even if the volumes gather pace, strong top-line growth will be hard to get. While Bata India products still deliver high quality, they lack freshness in design and offer lesser variety and lower style quotient. No doubt, Bata sells 47-48 million pairs in India but has lower profitability compared to close peer Metro Brands.

Metro Brands has surpassed Bata India in profitability front since 2021. While Metro Brands stock price has more than doubled, Bata India stock price has fallen 33% over the past two years.