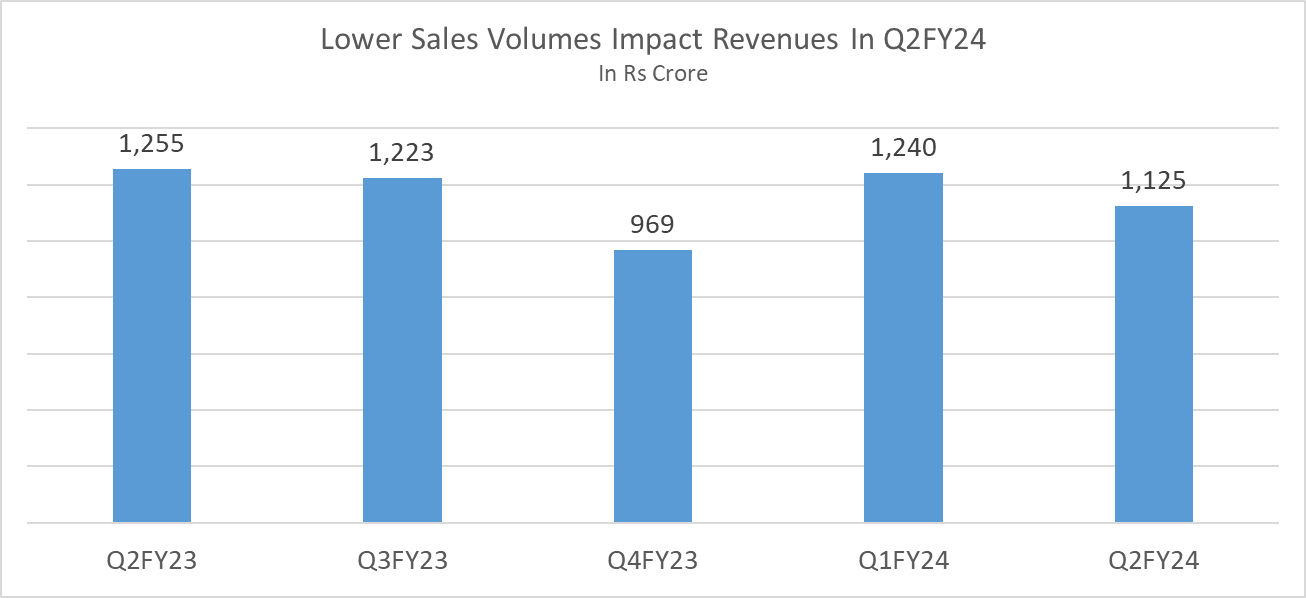

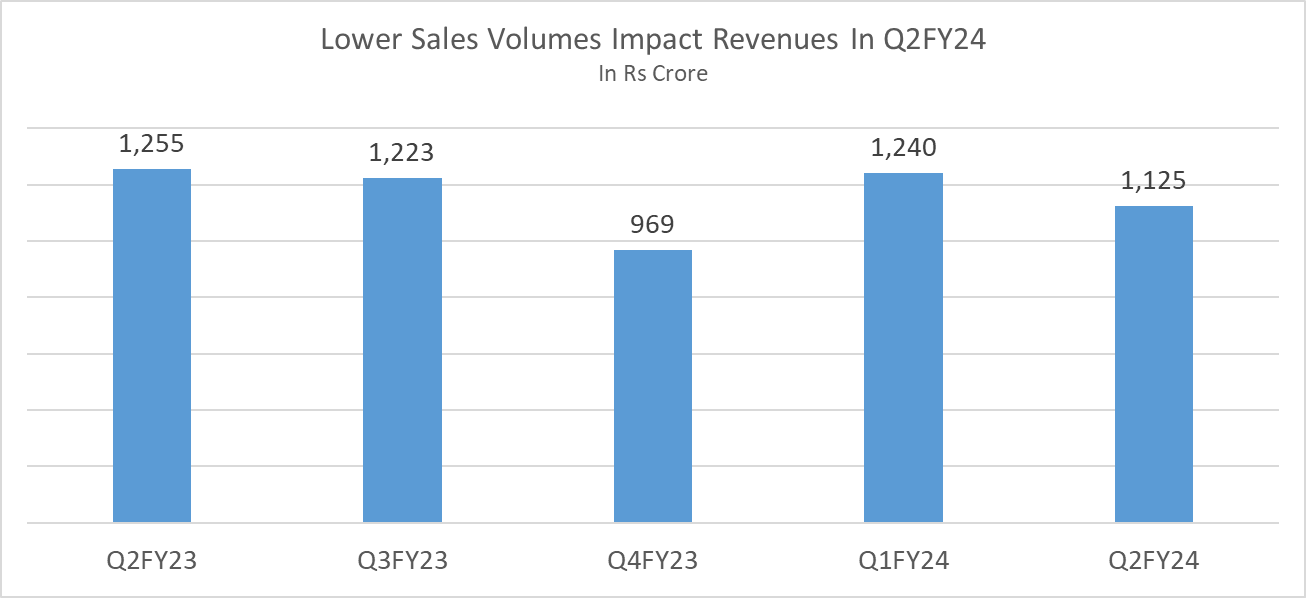

Page Industries stock price has fallen 20% over the past one year. Market leader of the Indian innerwear industry has reported negative revenue growth over the past three quarters. Page Industries revenues fell 10.3% YoY to Rs 1,125 crore in Q2FY24 compared to Rs 1,255 crore in the same period previous year. The company reported sales volume of 51.8 million pieces, lower by 8.8% YoY.

But despite lower revenues and volume growth, operating margins at 20.76% expanded 150 basis points (bps) YoY supported by operational expenses optimization and stable raw material costs. Speaking on margins, Deepanjan Bandyopadhyay, Chief Financial Officer at Page Industries said, “We are very comfortable in the range of 19% to 21%.” He further added, “And given all the operational cost optimization measures that we have taken and with the stability of the raw material costs, we are quite sure that this range will always be maintained.” And operating margins will be maintained despite higher investment in marketing and digital initiatives, the company intends to undertake in the near future. Net profit or profit after tax (PAT) came in at Rs 150 crore, a de-growth of 7.3% YoY in Q2FY24.

Speaking on September Quarter 2023 results, V.S.Ganesh, Managing Director at Page Industries said, “Demands in the innerwear and athleisure industry remained subdued in Q2FY24. This was in line with our anticipated expectations which contributed to lower sales volumes.” Lower growth is mainly attributed to subdued demand of innerwear across all categories and higher competitive intensity. The management is of the view that the customers have not downgraded their purchases. But the ticket size and frequency of innerwear has reduced. Speaking on lower volume growth and subdued demand, Ganesh said, “So there is generally a control on the spend, and we can see this across from the industry because many spends have gone up, the health, the education, rentals without a substantial increase in their salaries.” He further added that though positive trends were visible in economy and rural segments, urban and mid-premium are yet to witness improvement. The innerwear industry is also witnessing excess inventory accumulation owing to subdued demand across innerwear, athleisure and thermal categories. All brands have adopted deep discount practices to clear excess inventory. “Our industry has witnessed an accumulation of excess inventory, which has had repercussions on the overall ecosystem, resulting in certain unsustainable business practices in the market”, said Ganesh. The company however is not adopting unsustainable business practices but is working on optimizing its inventory levels. Inventory days have improved to 105 days in Q2FY24 from 150 days at the end of Q4 FY23. According to the management, the bloated inventory is now normalized as higher focus was given by the sales team on secondary sales. Speaking on inventory correction, Ganesh said, “Secondary sales have been slightly better than primary. See, we have actually crossed that bridge. And that’s where I’m saying the inventory correction is happening.” While innerwear players are trying to manage excess inventory, strong and stable demand trends are still awaited. On muted demand, Ganesh quipped, “We are very sure this is not going to be a long-term thing. And we can already see that this can’t last longer, and we are prepared to encash when the opportunity comes.”