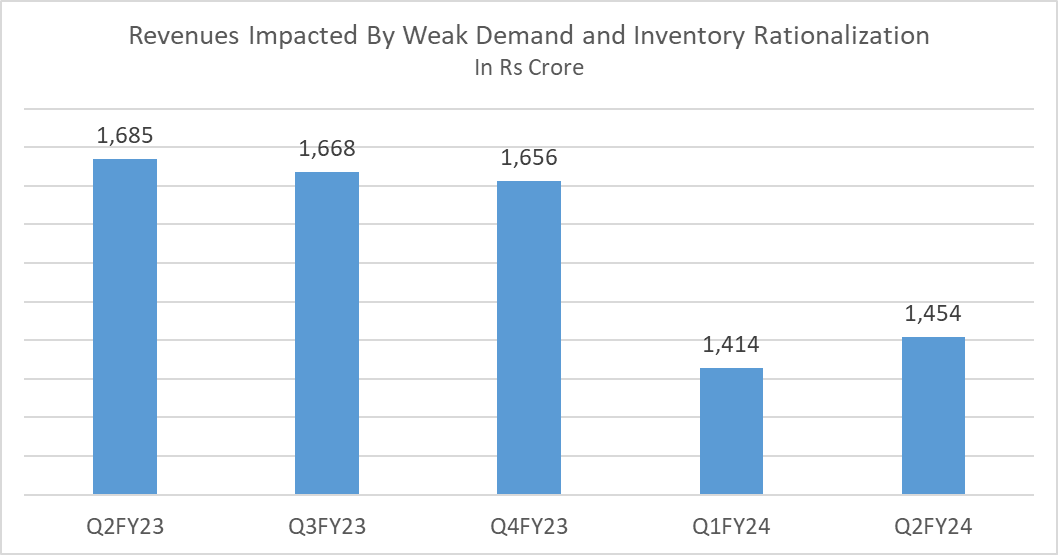

Aarti Industries Limited (AIL) is a leading Indian manufacturer of speciality chemicals and pharmaceuticals. The company has more than 100 products and more than 1,100 customers spread across the globe in 60 countries with major presence in USA, Europe, Japan. AIL manufactures speciality chemicals and intermediate for pharmaceuticals, agro chemicals, polymers, pigments, printing inks, dyes, fuel additives, aromatics, surfactants and various other speciality chemicals. The company reported subdued September Quarter 2023 with revenue falling 14% YoY and net profit declining 27% YoY. Revenue and net profit came in at Rs 1,454 crore and Rs 91 crore respectively in Q2FY24.

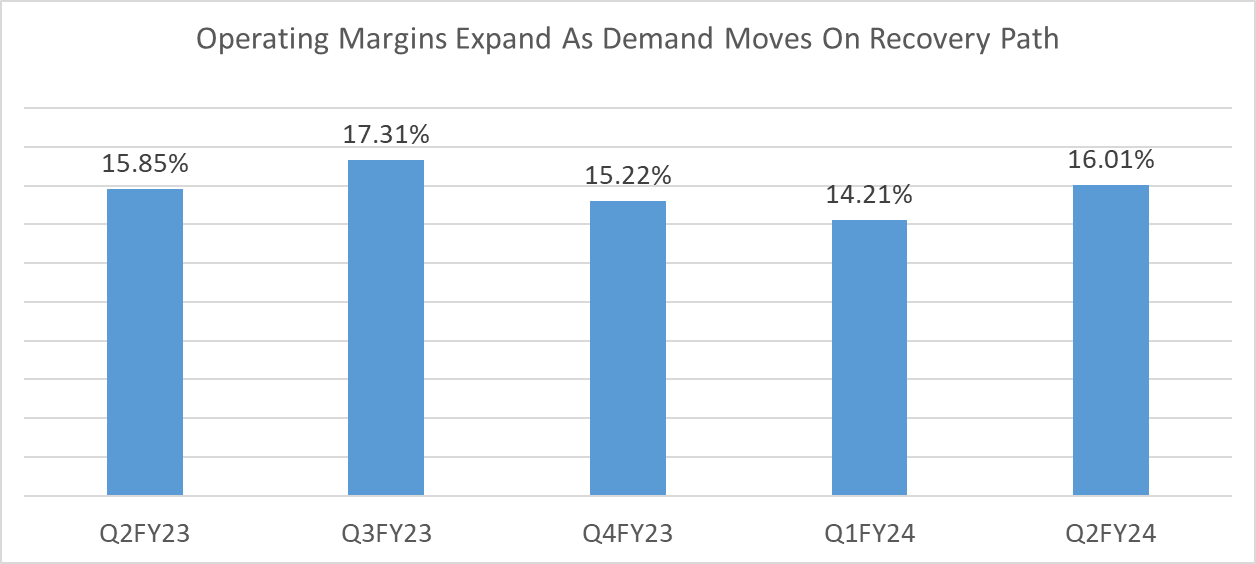

Operating margins stood at 16.01% in September Quarter 2023 compared to 15.85% in the corresponding quarter previous year. Speaking on mild margin increase, Rajendra Gogri, Chairman and Managing Director at Aarti Industries said, “Specific product-to-product where some demand increases, stabilization is taking place, there is some sort of a margin increase, is what we have observed.” He further added that margins will be sustainable at these levels in Q3FY24.

New projects, strong capex and Chinese competitive intensity to reduce

AIL has expanded Nitrochloro benzene capacity and ramp up is also expected to happen. According to the management, another major project of ethylation and NT expansion will get commissioned in FY25 and some debottlenecking will also be undertaken. The company is deploying capital expenditure (capex) of Rs. 2,500-3,000 crore over a two-year period, anticipating rapid growth in the foreseeable future. During the six-month period, capex of Rs 575 crore was spent across various expansion initiatives. The annual capex is in the range of Rs 1200-1300 crores for FY24. Along with demand revival, Gogri also expects Chinese competitive intensity to reduce in the near future. He further added that global demand will gradually recover in the next 2-3 quarters and will subdue high Chinese competitive intensity (aggressive pricing) which has impacted topline growth.

Green shoots in pigments and dyes, new agrochemicals contract to support growth

According to the management, demand in discretionary products such as dyes, pigments, polymers is seen in Q3FY24, but agrochemicals are still more molecule-specific. As crude prices rose during July-September 2023 period, pigment and polymers restocking was witnessed globally. Speaking on recovery Gogri said, “We have observed some recovery in dyes, and few specialty applications, while other end-user segments are yet to recuperate. We expect the worst to be over in H1 FY24 and anticipate that it will take a few more quarters for normalised demand across various end segments/product lines.” The company expects better performance in H2FY24 and foresees FY25 to be a normalising year with respect to the current pace of recovery. And positive growth is definitely on the cards as the company signed a nine year contract with a global Agrochem major for a niche agrochemical intermediate with a revenue potential of over Rs 3000 crore. According to the management, its existing manufacturing locations are sufficient to meet this contract requirement and the company does not anticipate any additional CAPEX for this. The global agrochemical market is valued at US$ 74 billion and is growing at a CAGR of about mid to high single-digit.