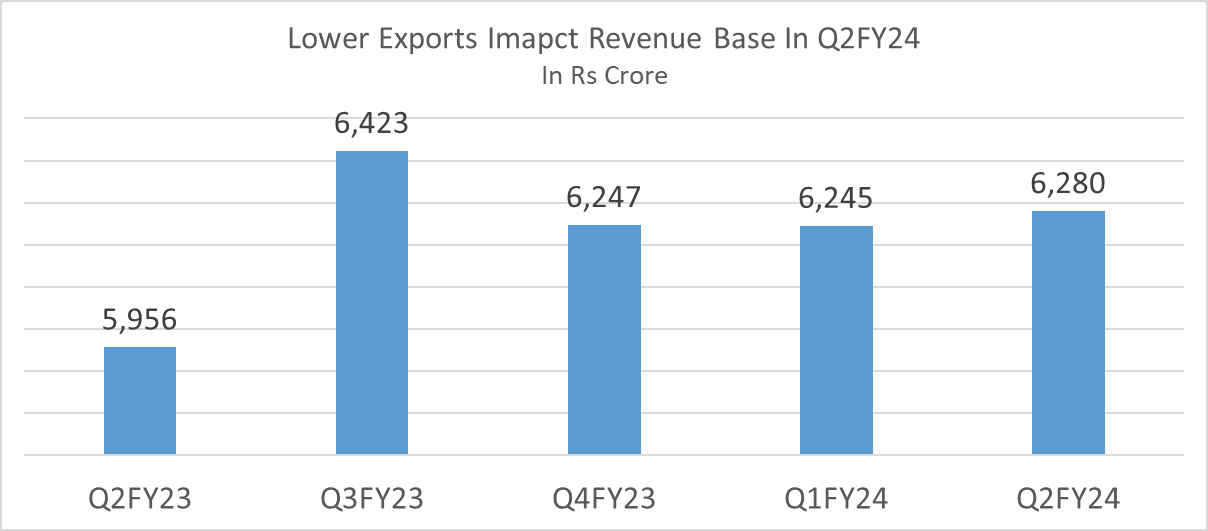

Apollo Tyres beat street estimates reporting strong operational performance in Q2FY24 driven by Indian operations. Apollo Tyres delivered resilient numbers despite a steep decline in exports in Q2FY24. The company witnessed export volume decline of 40% YoY in Q2FY24, but which is up 7% sequentially. Speaking on lower exports volumes, Gaurav Kumar, Chief Financial Officer at Apollo Tyres said, “Our top line growth in the domestic market should start improving with the domestic volume being up in double digits compared to last year.” Indian markets reported revenues of Rs 4,407 crore up 4% YoY with operating margins of 19.1% expanding more than eight percentage YoY. According to the management, overall volumes in India were up, with both OEM and replacement segment volumes growing in healthy double digits. But domestic volume growth was partially negated by steep decline in exports in Q2FY24. Strong volume growth in the domestic market was inspite of no price action taken by the company in September Quarter 2023. The management increased prices in the truck bias category which were later reduced due to competitive pressure. Overall revenues came in at Rs 6,280 crore up 5.4% YoY in September Quarter 2023.

Europe bottomed out, recovery expected in near term

Though European markets (28% of total revenue mix) are still not out of the woods, volumes have bottomed out. According to the management, European markets remained subdued with the industry volumes in passenger car and truck declining by 7% and 9% YoY. Apollo Tyres reported 6% YoY fall in revenues in euro terms. Revenues came in at 169 euros in Q2FY24 compared to 181 euros, same period previous year. Operating margins stood at 14.1%, a fall of 119 basis points (bps) YoY in September Quarter 2023. Speaking on European markets Kumar said, “We continue to focus on the product mix with the ultra-high performance (UHP) proportion being around 40%. The market is beginning to look better as we move into the third quarter.” According to the management, positive growth is expected in both passenger cars and commercial vehicles in the near term. “As far as Apollo truck bias radial (TBR) is concerned, we’ve already started seeing that there is a very good pull for our brand coming up. So, we believe that even in the CV cycle in Europe”, said Neeraj Kanwar, Vice Chairman and Managing Director at Apollo Tyres. The passenger car tyres were down during the quarter due to gap of certain sizes which are now being manufactured in India. Kanwar expects a surge in passenger car tyres in the near future.

Focussed more on margins than topline, no capex for next 2 years

“I’m not so concerned about top line”, said Kanwar as Apollo Tyres is focussing on EBITDA margins and balance sheet ratios. The company is not going for value volume products. Speaking on profitable growth, Kanwar said, “We are very clear we are going only after those markets, channels of distribution, which are going to be profitable to the company, whether it is in India, Europe, etcetera.” Operating margins stood at 18.5% in September Quarter 2023 expanding more than six percentage points aided by sales mix, benign raw material costs, and tight control over costs.

The company is also more focussed on investing in research and development (R&D) than incurring capital expenditure. Apollo Tyres invests 2.5-3% of its sales on R&D. The company also aims to be capex light for the next two years. Apollo Tyres has two digital innovation centers in the UK and Hyderabad, where data scientists analyse data and work along with the plants to increase production from the current equipment with small amounts of capex.