Polycab delivered the highest ever quarterly profit after tax (PAT) in September Quarter 2023. Revenues were up 27% YoY accompanied by 59% growth in net profit or PAT in Q2FY24. While management is confident of strong growth momentum driven by India’s ongoing infrastructural growth story, investors are awaiting its fast moving electrical goods (FMEG) segment to return to profitability. Polycab stock price gained 45% over the past one year.

Robust September Quarter 2023

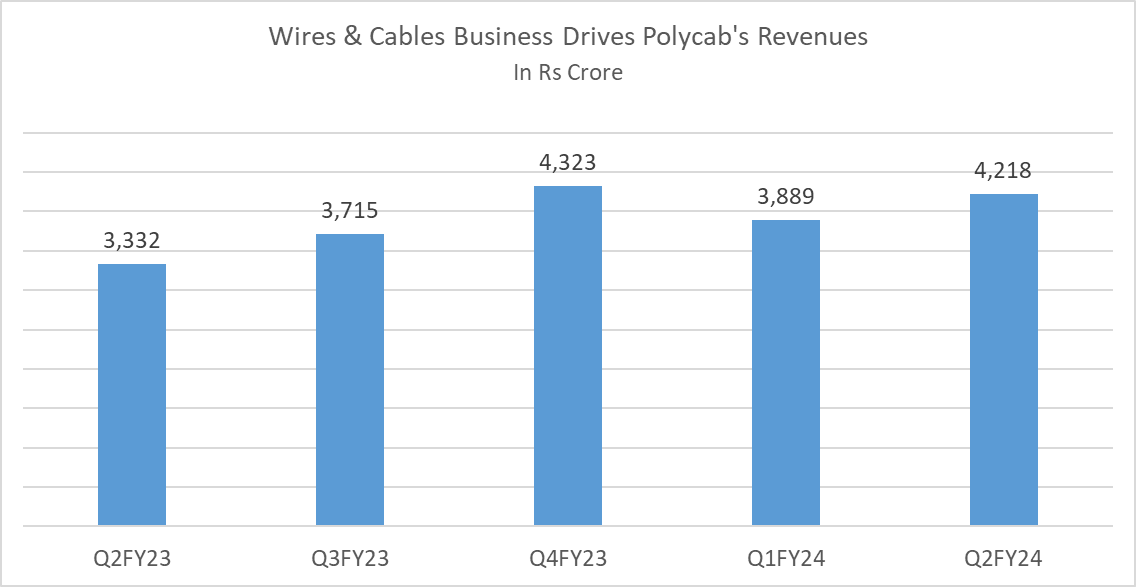

Revenue from operations came in at Rs 4,218 crore compared to Rs 3,332 crore, a rise of 27% YoY and 8% sequentially. Robust revenue growth was driven by the wires & cables (w&c) segment which constituted 89% of the total revenue mix in Q2FY24. W&C revenue at Rs 3,740 crore grew 28% YoY on the back of strong volume growth.

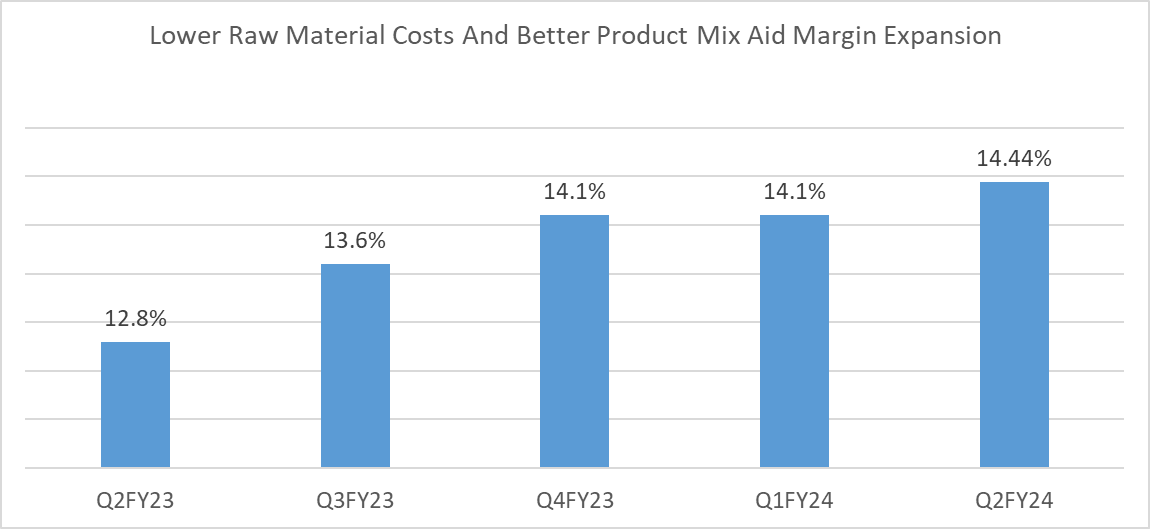

Operating margins stood at 14.44% expanded 160 basis points YoY in Q2FY24. Speaking on strong operating margin performance, Chirayu Upadhyaya, Head Investor Relations at Polycab said, “Margin expansion was achieved through enhanced operating leverage and a favourable product mix.” Embedded derivatives in raw material supplier contracts enable commodity price increase a complete passthrough to customers leading to stable margins. Robust top-line and strong margin expansion led to highest ever net profit growth of 59% YoY at Rs 426 crore in September Quarter 2023.

Wires & cables – pedal firmly on growth

Wires & cables revenues at Rs 3740 crore are up 28% YoY and 7% sequentially in September Quarter 2023. Cables and wires business reported robust volume growth of 30% YoY and 20% YoY respectively in Q2FY24. According to management demand was seen across all segments particularly infrastructure, largely driven by the government capital expenditure (capex). Government’s capex includes roadways, highways, railways, and metro line projects. And also from power transmission, distribution, real estate and defense sector. “Geographically, the growth was broad based, with highest growth coming from the northern region from states of Uttar Pradesh, Delhi and Haryana”, said Upadhyaya. The company pursued a targeted approach in the southern region which led to 19% YoY growth in Q2FY24 especially from key states such as Karnataka, Telangana and Tamil Nadu. But will this growth momentum be maintained with the general elections due in April 2024.

Irrespective of general elections in the next six months, the management is confident of sustaining double-digit volume growth. Speaking on infrastructure capex, Upadhyaya said, “Of course, the caveat being that the current government comes back to power. But at our end, we do believe that this is something which is a structural story and structural demand driver for the country.” He further added that, “Based on the demand that we are seeing on the ground, the volume growth in the industry has been better than what it has ever been.” And the management expects growth momentum to continue both from the government and private investment.

When will FMEG turn profitable?

FMEG segment reported revenues of Rs 328 crore up 8% YoY and 5% sequentially in September Quarter 2023. But there is loss of Rs 60 crore before interest and tax (EBIT) and EBIT ratio at -1.8% in Q2FY24. FMEG business was muted during the quarter as weak consumer sentiment weighed down on sales especially fans and lights segment. Fan segment was impacted by changes in Bureau of Energy Effeciency (BEE) norms mandated by the government. With strong optimism, Upadhyaya said, “This is the first year post those energy norms. The coming season will be the first year post BEE changes, and we should have good pickup as the season begins from October or November of this year.” Light segment has been impacted by price corrections undertaken by the company to the tune of 10-12% in Q2FY24. According to the management, pricing corrections have bottomed out and growth will recover in the near future. On the other hand switches reported an impressive sales growth of nearly 2x over Q2FY23. The management is confident of strong revival in FMEG business and is working on brand positioning and product development. The management is also making efforts to augment switch and switchgear business which has lower competitive intensity and higher margins. With product mix shifts from fans and lights towards switch and switchgears, margins and profitability will improve. Margins will also improve by scaling up FMEG business, said Upadhyaya. As operating capacity increases, costs reduce and operating margins improve. And lastly premiumization which will also aid both topline growth and higher margins. On premiumization, Upadhyaya said, “In all the product categories, we are trying to be present on the premium side, wherein, again, the margins are better.” By making these efforts, the management aims to achieve EBDITA of 10% for FMEG business by FY26.