Federal Bank reported healthy September Quarter 2023 with robust loan book growth and strong asset quality. The stock price touched its new 52-week high of Rs 152 before Q2FY24 results were announced. The private sector lender’s stock price has since then lost 2.6%.

September Quarter 2023 results looks impressive, highest ever net profit and net interest income (NII), robust loan book and stable asset quality. Speaking on strong Q2FY24 results, Shyam Srinivasan, Managing Director and Chief Executive Officer, Federal Bank said, “Sigma of all our initiatives taken over the past 6-7 quarters have come together in Q2FY24”. While the Federal Bank is slowly and steadily ticking all the right boxes, there is still a lot of work to be done. Balance sheet looks strong, but CASA (current account and savings accounts) ratio is falling over the past 5-6 quarters. Cost to income ratio is at its all time high and net interest margin (NIM) is witnessing a declining trend over the past three quarters. But let’s first unravel the main profitability and asset balance sheet parameters where the bank has scored remarkably well.

Robust loan book, stable asset quality in Q2FY24

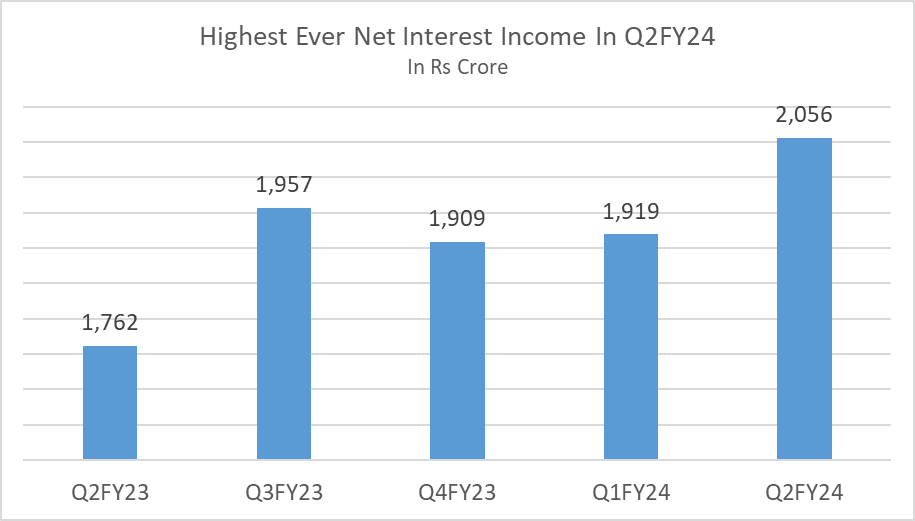

Net interest income (NII) grew 17% YoY to Rs 2,056 crore in Q2FY24 supported by growth in high yield loan book. High yield book constitute gold loans, personal loans, credit cards, commercial vehicle/commercial equipment loans and microfinance.

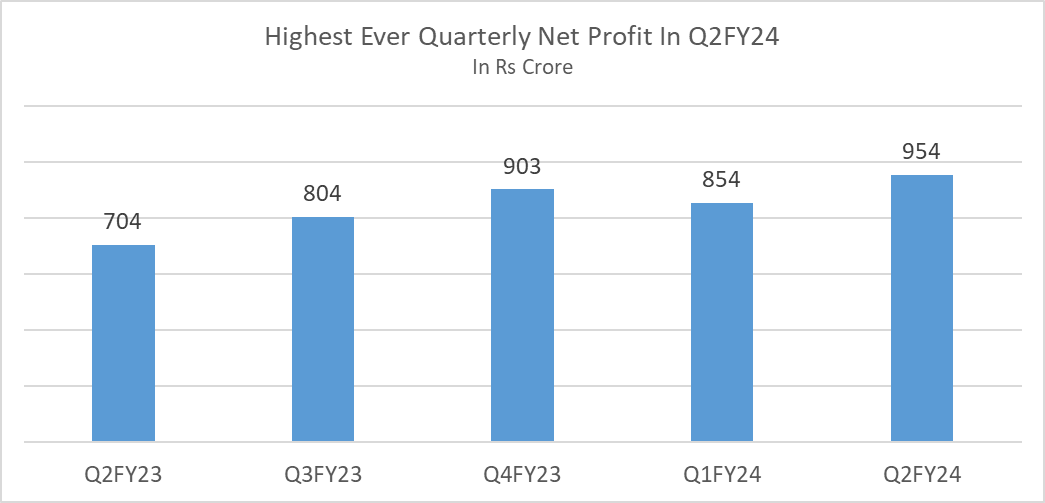

Profit after tax (PAT) or net profit came in at Rs 954 crore in September Quarter 2023 compared to Rs 704 crore in the same period previous year.

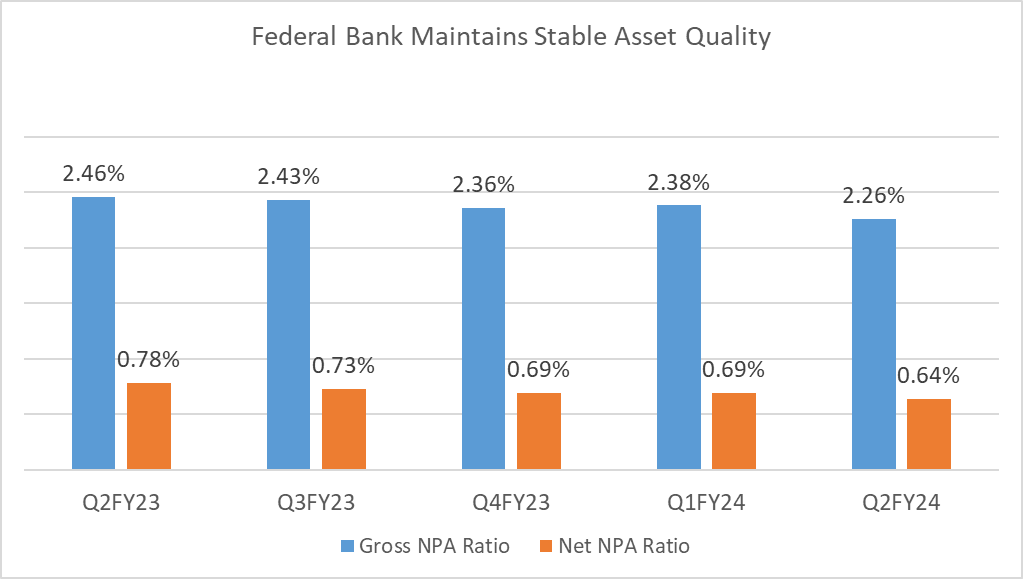

Asset quality was strong with improving gross NPA and net NPA ratio and lower provisions. Gross NPAs (2.26%) and net NPAs (0.64%) fell 20 basis points (bps) and 14 bps YoY respectively in Q2FY24. Gross NPA ratio was at its lowest in 34 quarters.

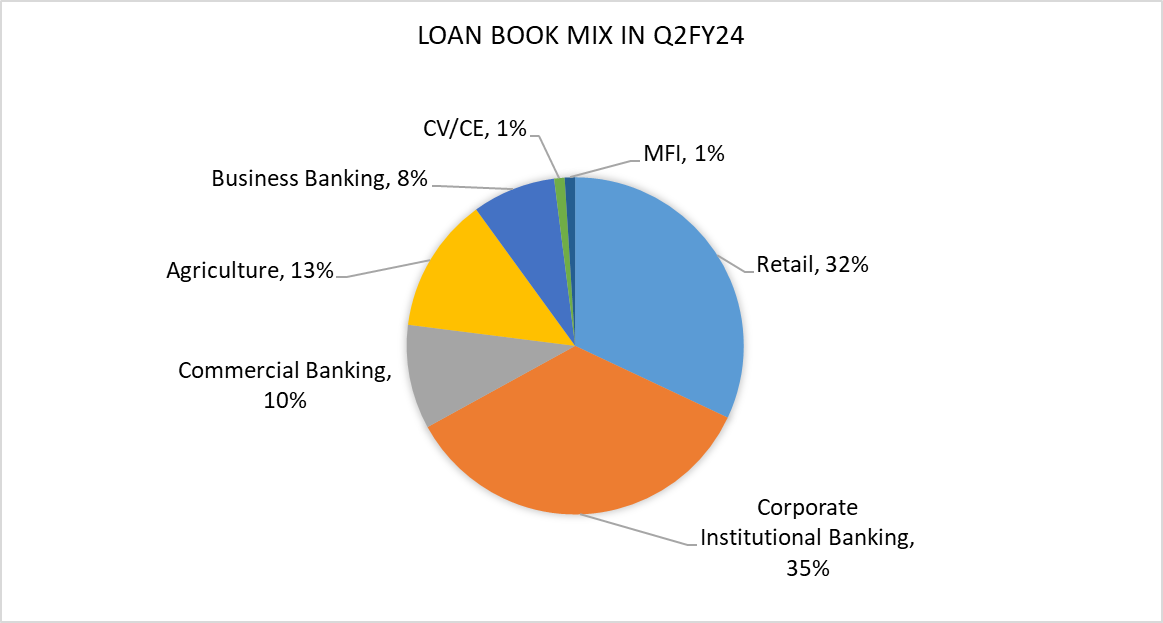

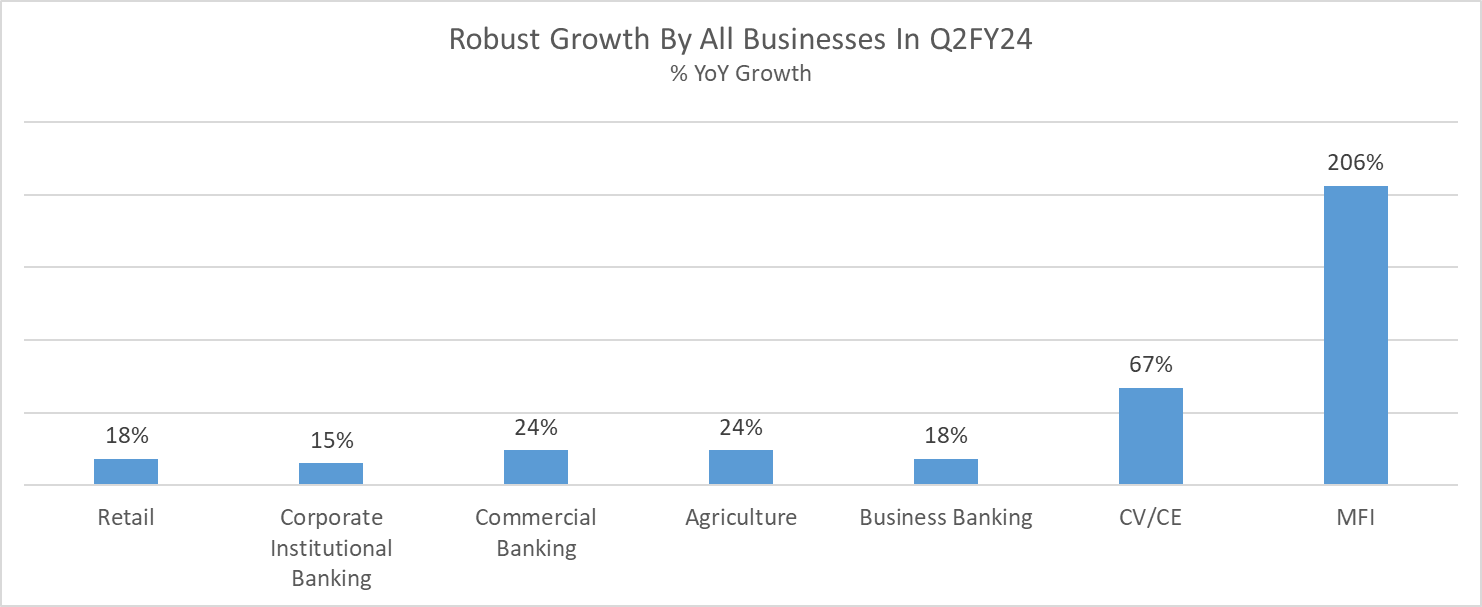

Provisions fell 27% to Rs 371 crore in Q2FY24 from Rs 509 crore, same period previous year. Credit cost is at its all time low of 13 bps (annualized), falling 40 bps YoY in Q2FY24 due to lower slippages and higher upgrades. Credit cost is the percentage of provisioning against total advances. A fall in credit costs enhances the lending capacity of banks. Coming to the loan book, Federal bank has outpaced industry credit growth (15%) and for the third consecutive quarter reporting 20% YoY loan book growth in Q2FY24.

And all loan segments have witnessed robust YoY growth in September Quarter 2023. This all looks good, but it is work in progress for Federal Bank.

High cost of deposits impact NIMs, cost to income ratio to improve in FY25

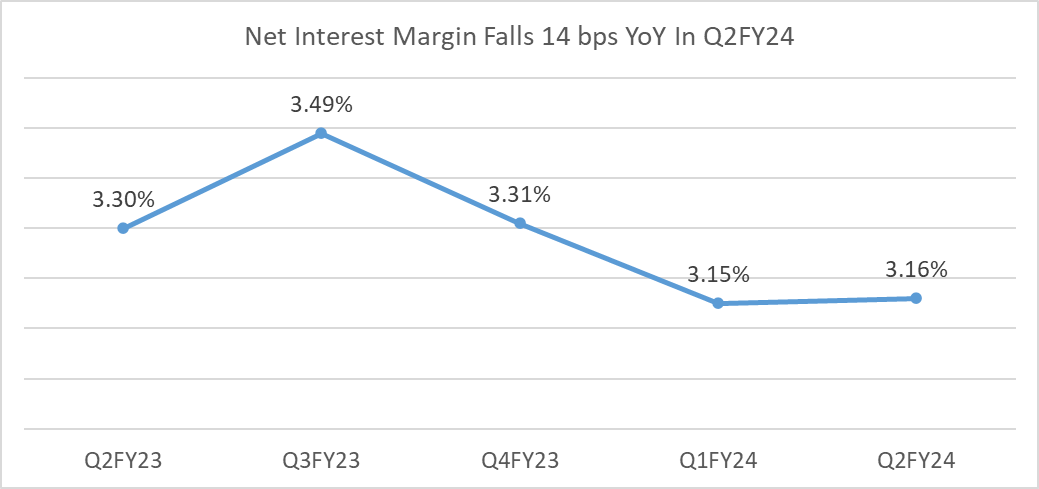

Federal Bank’s NIM has lost 33 bps since December Quarter 2022. NIMs (interest earned-interest paid/average interest earning assets) of the Indian banking sector are under pressure with rising cost of deposits.

Federal Bank’s yield on advances (interest earned) increased 106 bps YoY and cost of deposits (interest paid) rose 116 bps YoY in Q2FY24. Speaking on higher cost of deposits, Srinivasan said, “Money is available in the system, but at a higher cost. We should factor in 18-20 bps increase in cost of deposits in the near term”. He further added that the bank is using alternate sources of funds to ensure that the blended cost of funds is in control. The management has guided NIMs of 3.25% by the end of FY24.

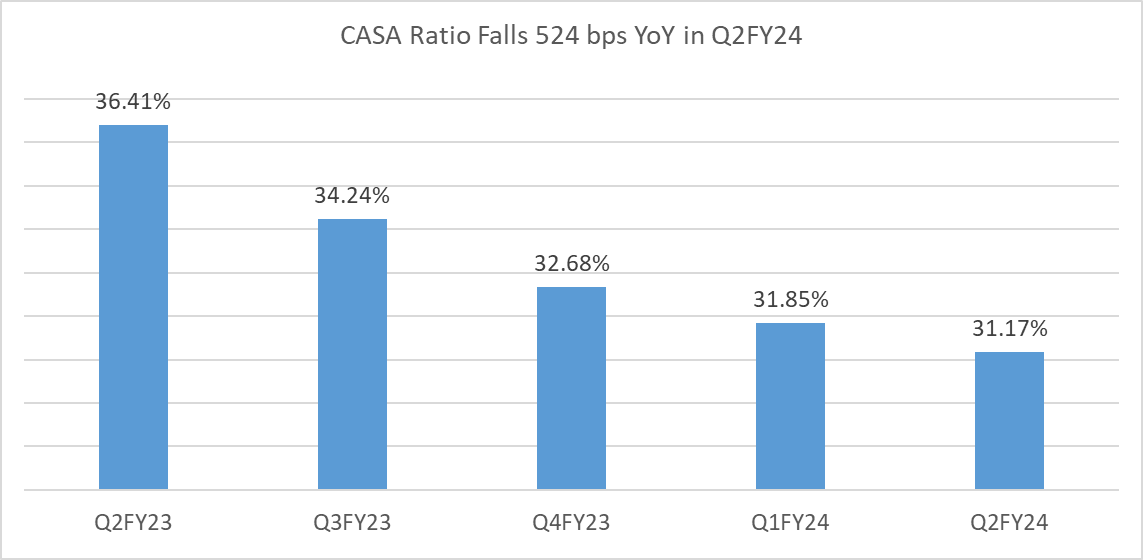

Cost of deposits is higher for a bank which has a lower CASA ratio. And Federal Bank’s CASA ratio has fallen five percentage points YoY in Q2FY24. CASA is low-cost deposits garnered by the bank by paying an interest rate as low as 3%. Higher repo rate has led to tightness in the banking system, where banks are competing with each other for deposits by raising interest rates for fixed and term deposits. Thus, even if Federal Bank’s total deposits (Rs 2,32,868 crore) have gone up by 23% YoY in Q2FY24, CASA deposit ratio (33.17%) is low with major contributions by term and fixed deposits leading to higher cost of funds. Federal Bank needs to augment its CASA customer base to lower its cost of funds and improve net interest margin trajectory.

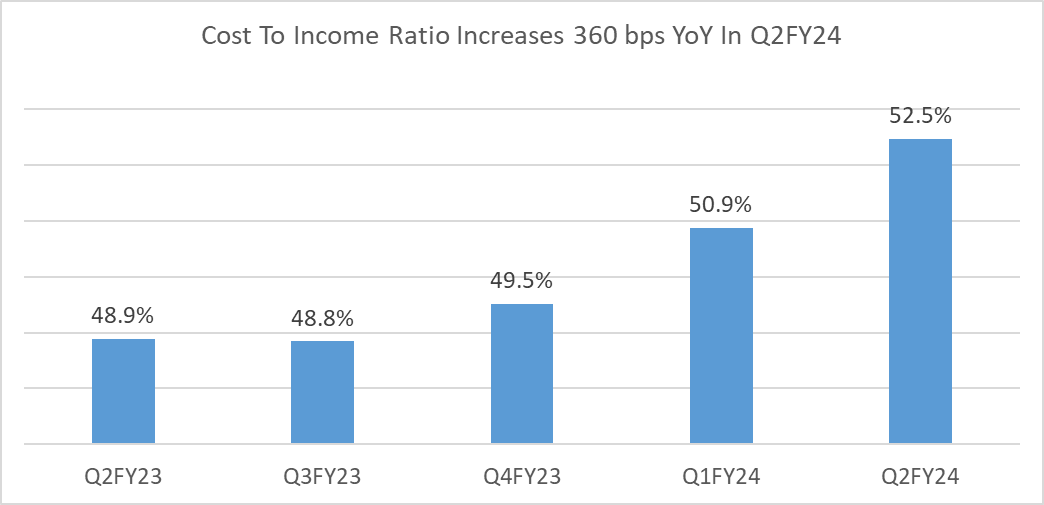

And lastly cost to income ratio is at an all time high of 52.47%, up more than three percentage points YoY in Q2FY24. Cost to income ratio (non-interest expenditure/net total income) reflects the extent to which non-interest expenses of a bank makes a charge on its net total income. The lower the ratio, the higher is the efficiency of the bank.

According to the management, there are certain high yield businesses such as credit cards, personal loans and microfinance which require higher investments. Speaking on high cost to income ratio, Srinivasan said, “We have taken a conscious decision to do these business as they are ROA accretive. Our income is expanding, NII is expanding but cost is up”. In addition to this, expenditure on marketing and promotion and branch expansion also increased cost to income ratio in Q2FY24. The management is working towards bringing down cost to income ratio and aims to reduce it to 50% by FY25.