Bata India stock price is up 6-7% over the past two days. A possible tie up with Adidas is in the works according to a CNBC report. After falling 3% intraday post muted Q1FY24 results, a possible Bata-Adidas deal reared up Bata India stock price which was down 11% till August 14, 2023. It’s a relief for Bata investors concerned about muted revenue growth, the franchise model yet to deliver visible results and consistent underperformance by the affordable mass footwear segment.

Muted June Quarter 2023

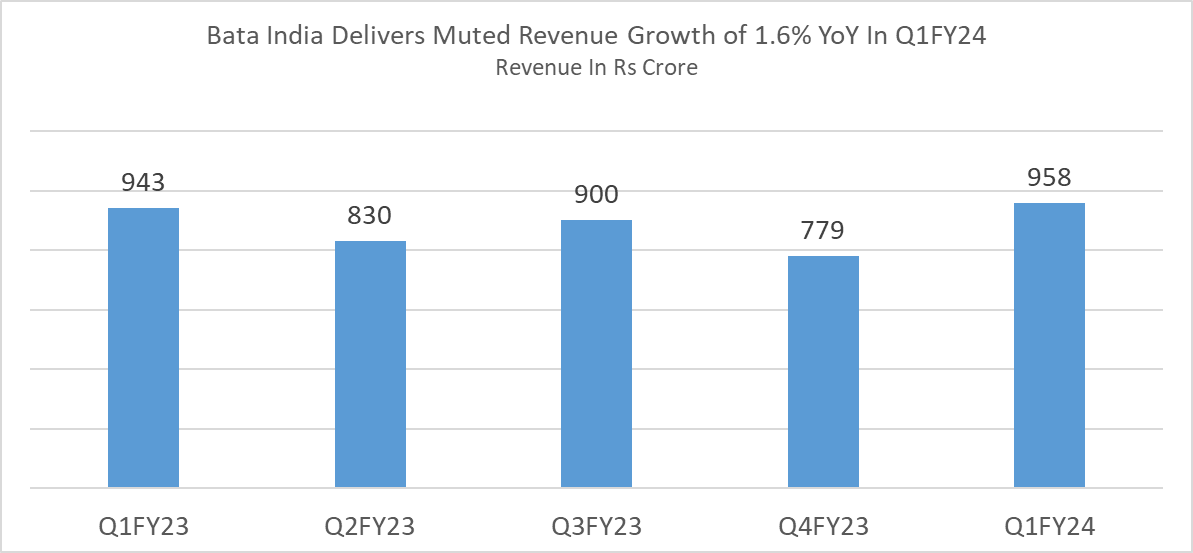

Revenue from operations grew 1.6% YoY in June Quarter 2023, lowest over the past nine quarters due to high inflationary pressures. No price hikes over the past 8-9 quarters, flat volumes YoY and reduced number of wedding days compared to the same period previous year impacted revenue growth in Q1FY24.

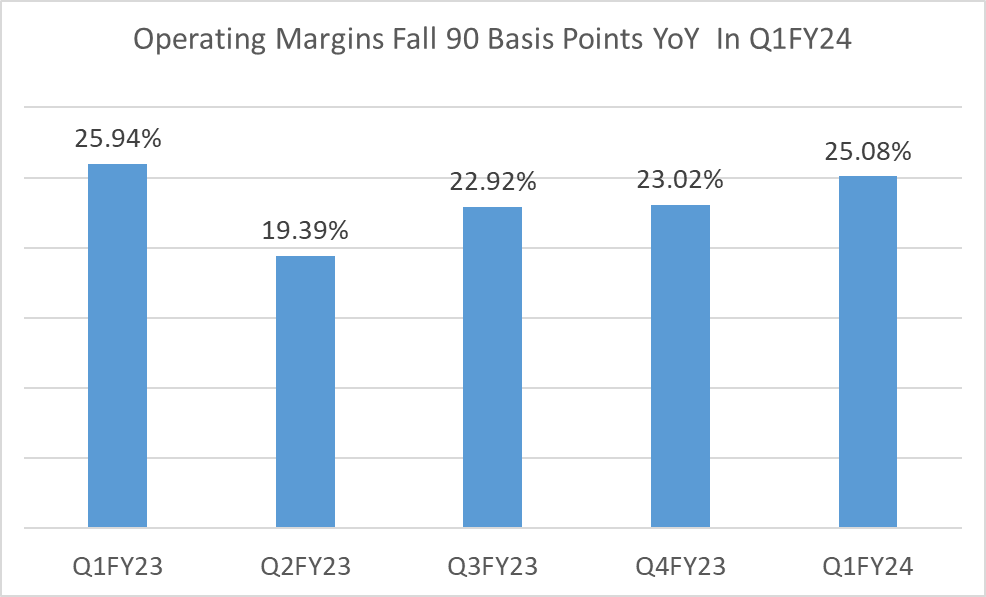

Amid a challenging demand environment, Bata India managed its margins well, reported at 25% in Q1FY24 contracting 90 basis points (bps) YoY. End of season sale (EOSS) in early Q1FY24 and inventory optimization impacted operating margins.

Net Profit fell 10% YoY in June Quarter 2023 to Rs 308 crore compared to Rs 292 crore corresponding quarter previous year.

Adidas to broaden Bata’s sneaker platform

‘Discretionary spend remains subdued in the footwear sector, prolonging the deceleration that started towards the end of March 2023’, said Gunjan Shah, CEO and Managing Director, Bata India. He further added that inflation is now stabilized and demand benefits are expected to flow in the upcoming festive season. Premium categories such as Hush Puppies and Comfit witnessed lower growth of 2% and 5% YoY respectively in June Quarter 2023. Premium category constitutes 30-35% of total turnover. Bata’s popular sneaker brand, North Star, reported decent double-digit growth of 15% YoY and Floatz growth doubled in Q1FY24. Sneakers currently contribute 20% of Bata’s total turnover and a strategic alliance or exclusive deal with Adidas would aid further premiumization enhancing average selling price (ASP) and augmenting volumes. What needs to be seen is whether the deal is an exclusive one, giving Bata, the sole distribution rights in India.

Re-imagining Bata through Adidas

Compound annual growth rate (CAGR) for revenue for the past three years is 4% for Bata India. Metro Brands CAGR stands at 19% for the same period. While Metro Brands is a premium footwear player, the mass category is a major growth damper for Bata India. Though it is not possible for Bata to exit mass category (below Rs 1000) completely like Metro Brands, product mix shift towards premium category with higher average selling price (ASP) is the way forward. With decades of leadership in the affordable mass footwear category (40-50% of turnover), the shift towards the premium segment will take time. The Adidas deal which is in the final stages would lighten some of the mass affordable category burden and increase youth connect and improve brand perception.

Bata’s retail network, a deal clincher

Bata India has been on an aggressive retail expansion over the past 5-6 quarters. Retail network comprising company owned and company operated (COCO), franchise and shop in shops (SIS) increased 16% over the past five quarters. The largest contribution was from franchise stores which increased 48% since March 2022.

The company aims to garner rural and semi urban demand through franchise model from Tier II-V cities which had been neglected for the past so many years. Adidas India would benefit from this huge retail network and penetrate into rural India. Hopefully, it should be both revenue and margin accretive for Bata India. The final contours of the deal would give a better picture.