Varun Beverages stock price has more than doubled over the past one year. Strong volumes, robust margins and consistent growth in revenues and profitability has stirred a strong investor interest in Varun Beverages Ltd (VBL).

While the Indian fast moving consumer goods (FMCG) sector reels under lower volume growth rate, VBL’s volumes are growing in strong double-digits. Will the robust volume growth slowdown in CY23 on a higher base or Sting’s consistent growth push VBL to scale new highs.

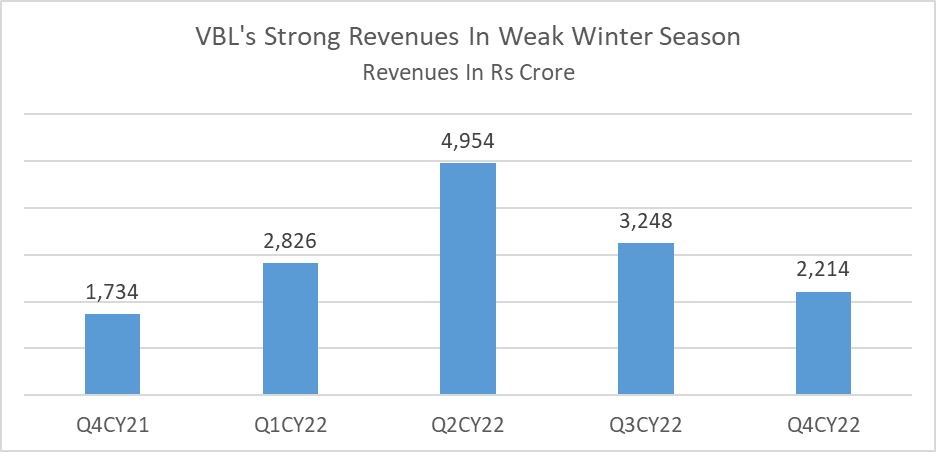

Strong volumes aid revenue growth, robust margins

Varun Beverages is one of the largest franchises of PepsiCo in the world (outside USA). VBL produces and distributes carbonated soft drinks (CSDs) and non-carbonated beverages (NCBs) owned by PepsiCo such as Pepsi, Diet Pepsi, Seven-Up, Mirinda, Mountain Dew, Sting, Tropicana juices and Aquafina, packaged drinking water.

The company reported revenues of Rs 2,214 crore in Q4CY22 compared to Rs 1,734 crore, a year ago, a rise of 27% YoY. Strong revenue growth was fuelled by distribution network expansion and post pandemic pent-up demand. Volumes increased 18% YoY to 132 million cases driven by strong growth in both Indian and international territories.

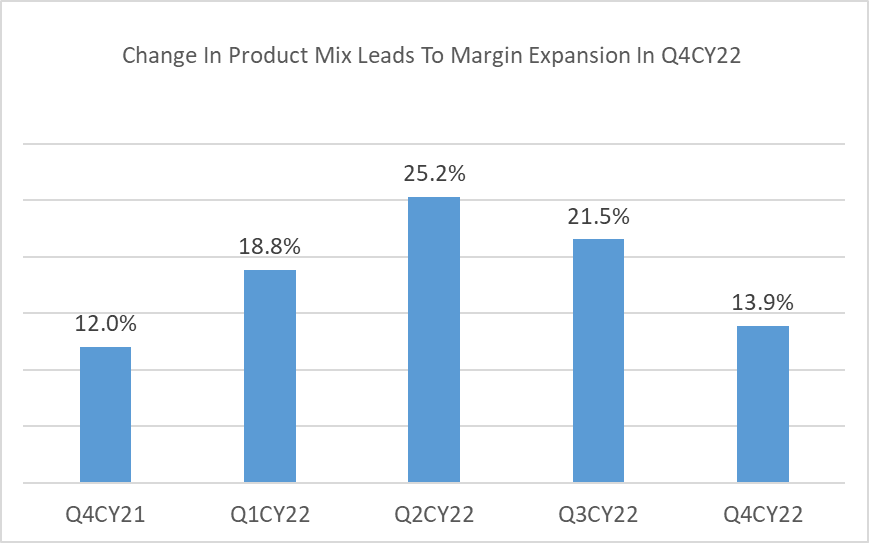

Operating margins came in at 13.89%, expanding 192 basis points (bps) YoY in Q4CY22. According to the management, despite inflationary pressures, early stocking of raw materials and change in product mix (higher Sting and lower water volumes) led to higher realization per unit and improved margins.

Net profit more than quadrupled to Rs 75 crore in December Quarter 2022 supported by higher revenue growth, improved margins, and lower tax rate.

Growth bole to Sting

For the health-conscious affluent urban millennials, tea, coffee are mild and carbonated drinks or alcoholic beverages are hazardous for health. Energy drinks have become popular among the young population in colleges, clubs and social gatherings. Energy drinks which mainly contain caffeine along with B-vitamins, herbs and amino acid derivatives (such as taurine) increase alertness of mind and enhance stamina. The Indian energy drink market has tripled in the past twenty years to Rs 2,200-2,400 crore in India.

Austrian based Red Bull is the market leader and the oldest player in the Indian energy market. Red Bull was launched in 2003. Energy drinks were premium products priced between Rs 110-130 for a 250 ml can till PepsiCo launched Sting in 2017 at Rs 50. Sting created its own affordable energy drink segment for price conscious college and office going youth. Sting’s 250 ml price was further reduced to Rs 20 in 2020 to take advantage of Red Bull’s supply disruption caused by Covid-19 pandemic. While Red Bull supplies are completely dependent on imports, Sting is manufactured and distributed in India by VBL.

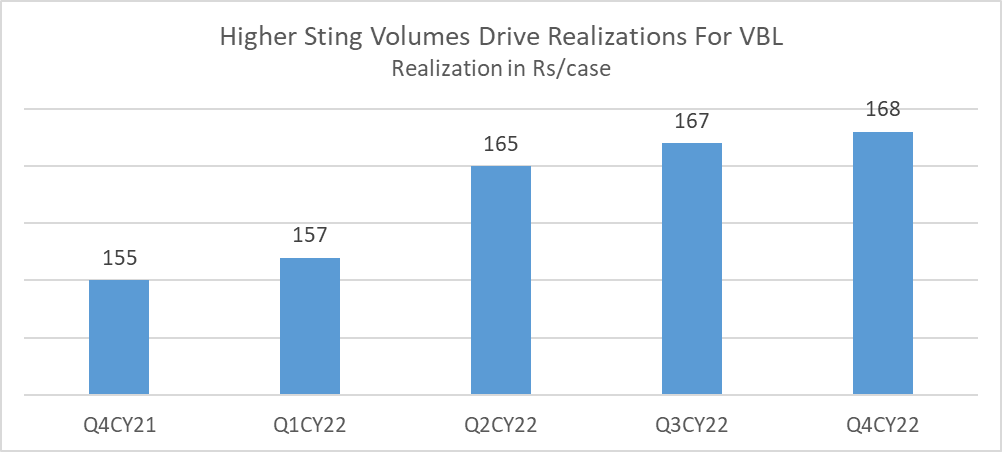

Covid disruption out of the way, Varun Beverages total volumes grew 41% YoY in CY22. In Q4CY22, volume growth was 18% YoY. Varun Beverages acquired south and western territories in 2019. With ceasing of Covid headwinds, fruits of expansion are now being availed after two years. In addition to this, with an improving power situation, cold drinks are now easily available in rural areas. While the rest of the FMCG pack is witnessing low rural volumes, Varun Beverages is growing strongly in rural India. Sting is a major driving force with its quarterly volumes rising 175% YoY in Q4CY22. VBL’s focus on small SKUs of 250 ml at just Rs 20 supported by strong distribution expansion aided Sting’s strong volume growth. Speaking on Sting’s growth, Ravi Jaipurua, Chairman at Varun Beverages said, “Sting contribution during the last quarter was much higher than the full year contribution of 10% in CY22. It went up to as high as 16% in Q4CY22.”

High proportion of Sting in the total volume mix has also aided higher realizations and margins. Sting’s realization is 65% more than other products.

Coca Cola has recently launched Thums Up Charged and other close peers Monster and Red Bull are expected to launch products in the affordable segment, but Sting has the first mover advantage. Whether VBL will be able to maintain Sting’s growth momentum and scale up its volumes further, the next few quarters will give a better picture.

The Campa Cola Jio Effect

Campa Cola was launched in the second week of March 2023. Reliance Retail Ventures launched Campa Cola’s 250 ml bottle at Rs 10. Coca Cola and PepsiCo’s products are available in 250 ml polyethylene terephthalate (pet) bottle packs at Rs 15. While Coke has denied reducing prices of 250 ml pet bottles and cans, price war is imminent with Reliance now in the Indian beverage industry. Though, the Indian beverage industry is characterized with high volumes and low price, distribution reach and outlet expansion is going to be the key factor to augment volumes and drive revenues. Varun Beverages needs to expand both its manufacturing facilities and distribution network to battle Campa Cola’s Jio effect.

Varun Beverages has 31 state of art production facilities, three million retail outlets, 2,400 primary distributors, 110 depots and 9,25,000 VISI coolers. The company plans to increase its retail outlets by 10-15%, close to 3.5 million in 2023. As outlets expand, distribution infrastructure such as vehicles, distributors, depots and VISI coolers will also increase proportionately. The company is also undertaking national rollout of its value-added dairy beverages (Cream Bell) and Tropicana fruit juice expansion next year. The capital expenditure (capex) for CY23 stands at Rs 1,500 crore. Speaking on VBL’s expansion plans, Jaipuria said, “Rajasthan and Madhya Pradesh are two greenfield projects and there is brownfield expansion at six additional plants spread across India.” VBL plans to increase its Indian volumes which are around 652 million cases by 50% over the next three years.

Campa Cola, even with Reliance Industries deep pockets and wide distribution network will take some time to gather reasonable market share in the Indian market. Varun Beverages, on the other hand, should execute its capex plans well. Any delay or failure to enhance its production capacities or augment its distribution network will be detrimental for future growth.