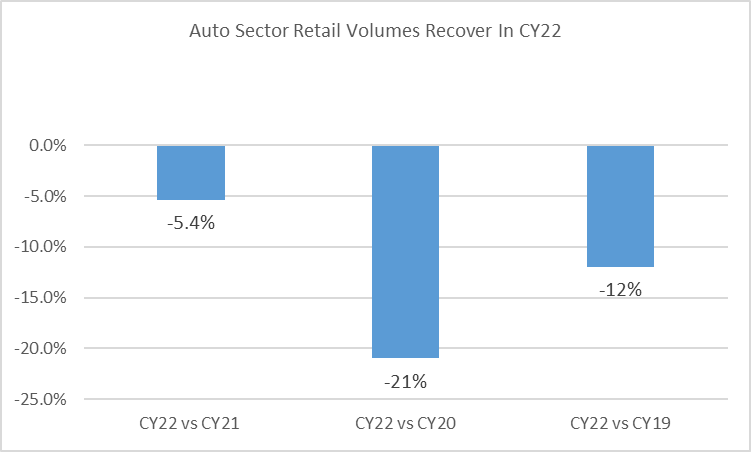

Nifty Auto is up 9.5% YoY. The auto sector is cyclical in nature. Automobile sales depend on expansion and contraction of the economy, interest rates, employment scenario and consumer sentiment. The Indian auto sector as per retail volume data from Federation of Auto Dealers Association (FADA) seems to be on a recovery path in CY22 vis-a-vis CY21.

But the real auto sector recovery can be rightly gauged in comparison to CY19, in absence of Covid-19 headwinds.

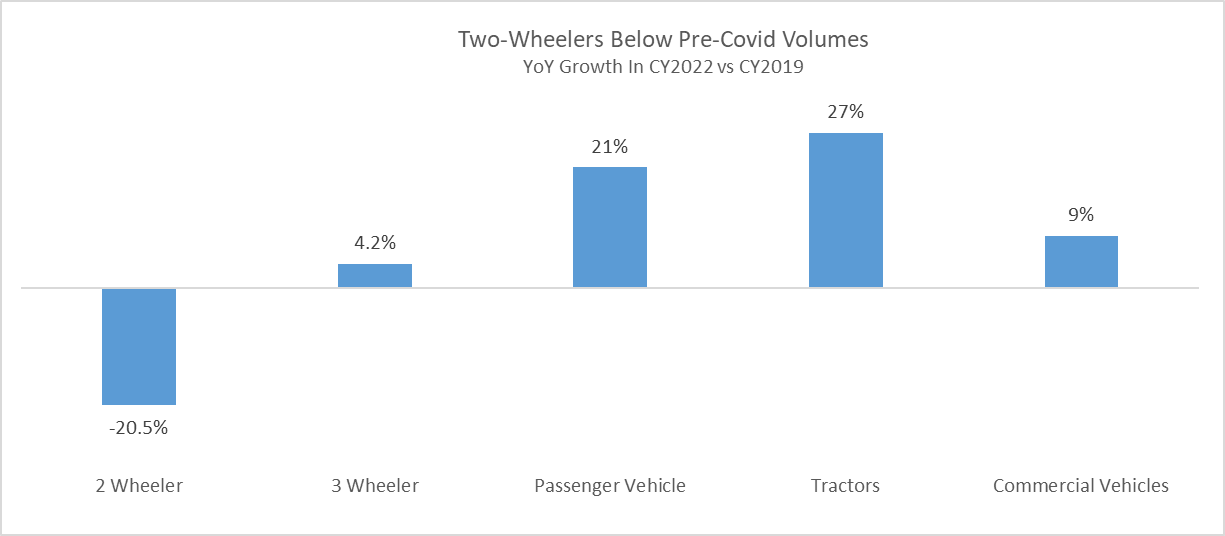

All the segments except two-wheelers reported strong positive growth in CY22 compared to CY21. In comparison to CY19 retail volumes, the two-wheeler segment is in negative terrain while all other auto segments, passenger vehicles (PV), tractors, three wheelers and commercial vehicles (CV) performed well in CY22.

Financial health of the base of the economic pyramid can be gauged by two-wheeler sales. In India, the two-wheeler segment is the largest segment constituting nearly 70% of total auto volumes with rural India as its major market. But the two-wheeler segment is vulnerable to economic cycles, rise in interest rates, state of rural economy and monsoons. If monsoons falter, lower disposable income in the hands of rural India impacts sales of motorcycles and scooters. Hero MotoCorp sells 70% of its volumes in rural India. Two-Wheelers reported positive retail volume growth only in the month of October 2022 compared to October 2019 spurred by festive fervor. And thus, the two-wheeler segment reported negative YoY retail volume growth in CY22 compared to CY19.

In contrast to this, passenger vehicles (PV), tractors and CVs have been the strongest segments throughout CY22. Passenger vehicle volumes were driven by compact sports utility vehicles (SUV) and SUV in CY22. The SUV segment currently contributes 40-45% of total PV volumes. PV segment constituted 16% of total retail auto volumes in CY22 and rose 15.6% in CY22 compared to CY19.

Post Covid-19 pandemic, the Indian agriculture sector has been impacted favorably. Increase in price of crops, higher minimum support price (MSP), good monsoons, reverse migration to rural India due to Covid-19, led to higher tractor sales. Tractors retail volumes increased 23% in CY22 compared to CY19 volumes.

Three-Wheeler is another significant category for the auto sector. Three wheelers enable least expensive last mile connectivity for both people and cargo. Electric three wheelers, known as E-Rickshaws currently have nearly 50% market share in the Indian three-wheeler market. While conventional diesel and petrol three-wheelers volumes have fallen, E-Rickshaw retail volumes have jumped strongly in CY22, propelling overall three-wheeler volumes to pre-Covid levels. E-Rickshaw volumes are driven by cost and fuel efficiency, no pollution and low maintenance.

Commercial Vehicles (CV) segment constitutes light, medium and heavy commercial vehicles such as vans, buses, trucks and construction equipment etc. CV retail volumes increased 9% in CY22 compared to CY19. The uptick in demand in this segment is supported by the government’s continued push for infrastructure development. While the CV segment is expected to do well in 2023, the PV segment might face headwinds. Higher base of CY22 and increased financing costs might slow down PV demand. But OEMs like Maruti Suzuki gunning for 50% market share in the Indian PV market is launching 2-3 SUV models in 2023. Tata Motors, the strongest player in the electric PV segment is also expecting strong sales in 2023 despite inflation and high base effect. Tractors are also expected to do well with strong government support on the agriculture front. E-Rickshaw onslaught on the conventional fuel three-wheeler market is also expected to continue. But for the Indian auto sector to rebound above pre-Covid volumes, the two-wheeler segment which constitutes 70% of total auto retail volumes needs to grow. And for that rural India needs to get back on the growth track.