Tata Consultancy Services (TCS) stock price fell 2% post its December quarter 2022 result announcement. Revenue growth came in at 19% YoY and net profit grew 11% YoY, but the street was not impressed. Nifty IT is the worst performing sector index down 26% YoY. While the present uncertain global macro-economic and geopolitical tensions persist, the Indian Information & Technology) (IT) sector is biding its time waiting for the tide to turn in its favour.

Stable numbers, lower constant currency growth

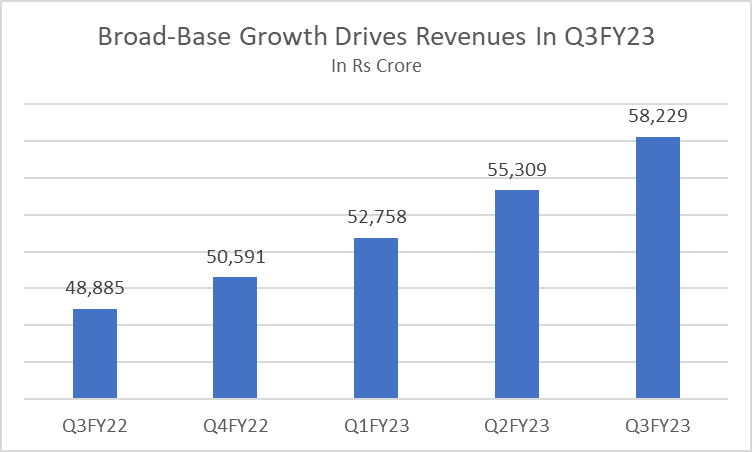

TCS revenues came in at Rs 58,229 crore up 19% YoY in December Quarter 2022 driven by broad based growth across all verticals.

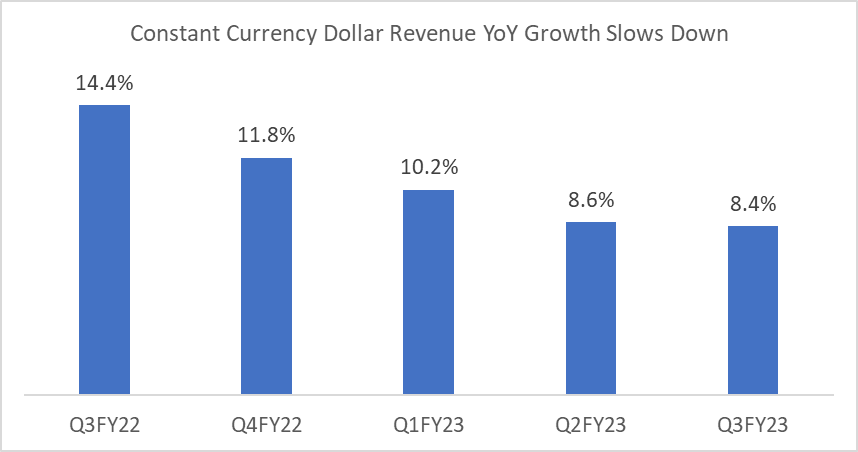

In dollar terms revenue growth at $ 7,075 million was up 8.4% YoY. In rupee terms, cc revenue growth was at 13.5% YoY.

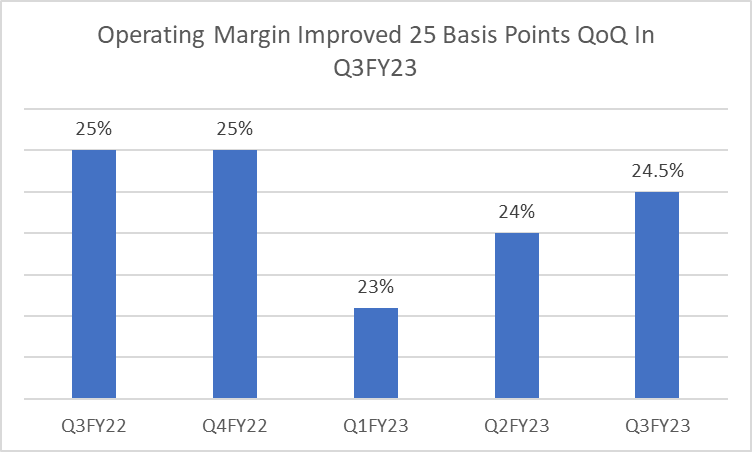

Margins came in at 24.5%,up 50 basis points (bps) sequentially in Q3FY23. According to the management, 100 bps benefit was derived from currency movement and lower sub-contracting costs which were partly offset by higher third-party expenses (30 bps).

Net profit crossed Rs 10,000 crore threshold for the first time in September Quarter 2022 and rose 4% QoQ reported at Rs 10,846 crore up 11% YoY in Q3FY23.

Elongated decision making and near-term uncertainty

Revenue growth of 19% YoY looks healthy for a seasonally weak December quarter due to furloughs and higher number of holidays. But investors also closely look at constant currency (cc) growth for export-oriented service sectors such as IT. The IT sector can either be adversely impacted or benefit from currency fluctuations. Thus, constant currency (fixed exchange rate) calculation helps in understanding the financial performance of a company without distortions caused by currency movements. TCS constant currency dollar revenue growth fell to 8.4% YoY from a high of 14.4%, a year ago.

In rupee terms also cc revenue YoY growth came in at 13.5% in December Quarter 2022 compared to 15.4% in Q3FY22.

The past 10-12 months have been tough for the Indian IT sector. As high inflation pushes central banks across the globe to increase interest rates, companies fear recession. Thus, companies have restrained IT spends, tightened budgets and delayed decision-making as IT expenditure is treated as discretionary expenditure. And this impact can be seen on TCS quarterly numbers.

North America, contributing 50.3% of total revenue basket, grew at 15.4% (cc) YoY in Q3FY23, slowing down from a high of 19.1% (cc) YoY in Q1FY23. While all other geographies have also witnessed revenue deceleration, the UK reported positive growth in December Quarter 2022 with revenues (cc) rising 15.4% YoY.

Speaking on geographic revenue contribution, Rajesh Gopinathan, CEO and MD at TCS said that the UK market is doing well and the decision-making process is fast. The company is on a wait and watch mode in the US market. “We think the immediate caution that is there, probably will dissipate a few months into the year”, said Gopinathan. Macro-economic uncertainties have led to cautious clients delaying decision making process and focussing on cost optimization deals. In the case of Europe, the decision- making process has also slowed down significantly according to the management. In case, the geopolitical situation calms down and decision-making restarts, the company expects to do well in Europe. The US and European market together accounts for nearly 70% of the revenue basket.

BFSI slows down, manufacturing recovers

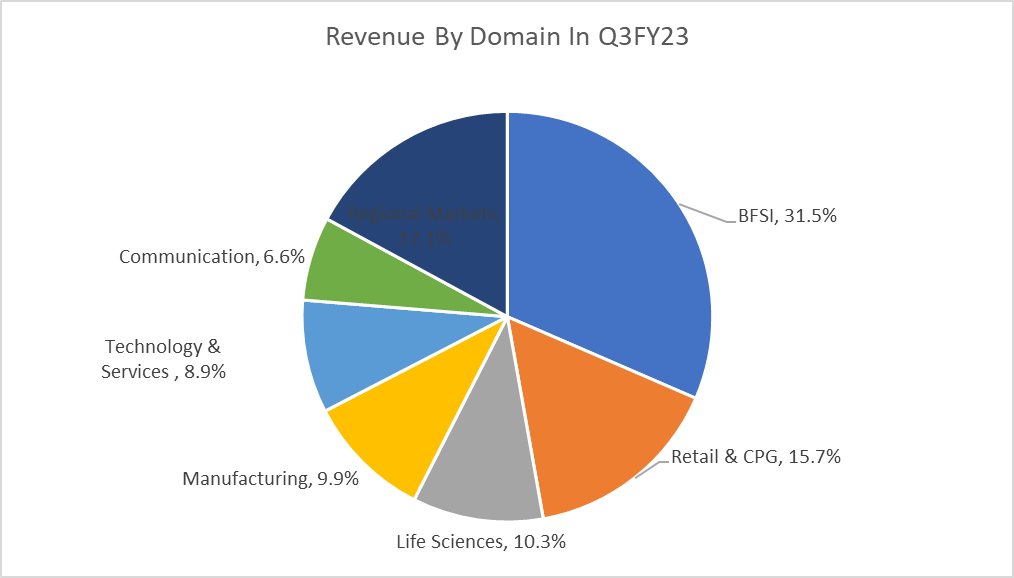

Banking and Financial Services Insurance (BFSI) sector contributes nearly one third of TCS revenues. While all other segments have also witnessed lower revenue growth, BFSI cc revenue growth slowed down significantly to 11% YoY in Q3FY23 from 17.9% YoY growth (cc), a year ago. Revenue growth by domain was led by retail & CPG vertical which grew 18.7% YoY, aided by the travel and hospitality segment.

While all verticals are expected to perform well, the management is cautious on manufacturing despite its resilient performance as global supply chain and energy price disruption might impact adversely.

TCS reported stable numbers amid slowing growth, but investors were unhappy due to lower constant currency growth and revenue deceleration in BFSI vertical and North American market. The stock price has regained over the past one week. The management’s positive commentary reassured investors. Gopinathan said that IT is no more discretionary but an industrial perennial. Upgrading IT infrastructure, cloud investment and cyber security needs are now recession proof non-discretionary IT spends. The deal closures for TCS in Q3FY23 amounted to a total contract value (TCV) of $7.8 billion. Despite inflationary pressures and geo-political tensions, robust TCV indicates the company’s strong ability to book future revenues. The management expects its industry leading margins to expand further and accelerate its constant currency revenue growth rates back to double digits in the medium term.

The latest US inflation rate at 6.5% is soothing both for the US Fed and the investors. While inflation is still above targeted 2%, the US Fed might take slower interest rate hikes saving the US economy from barging into recession. The tide has just started turning.