Suhani Adilabadkar

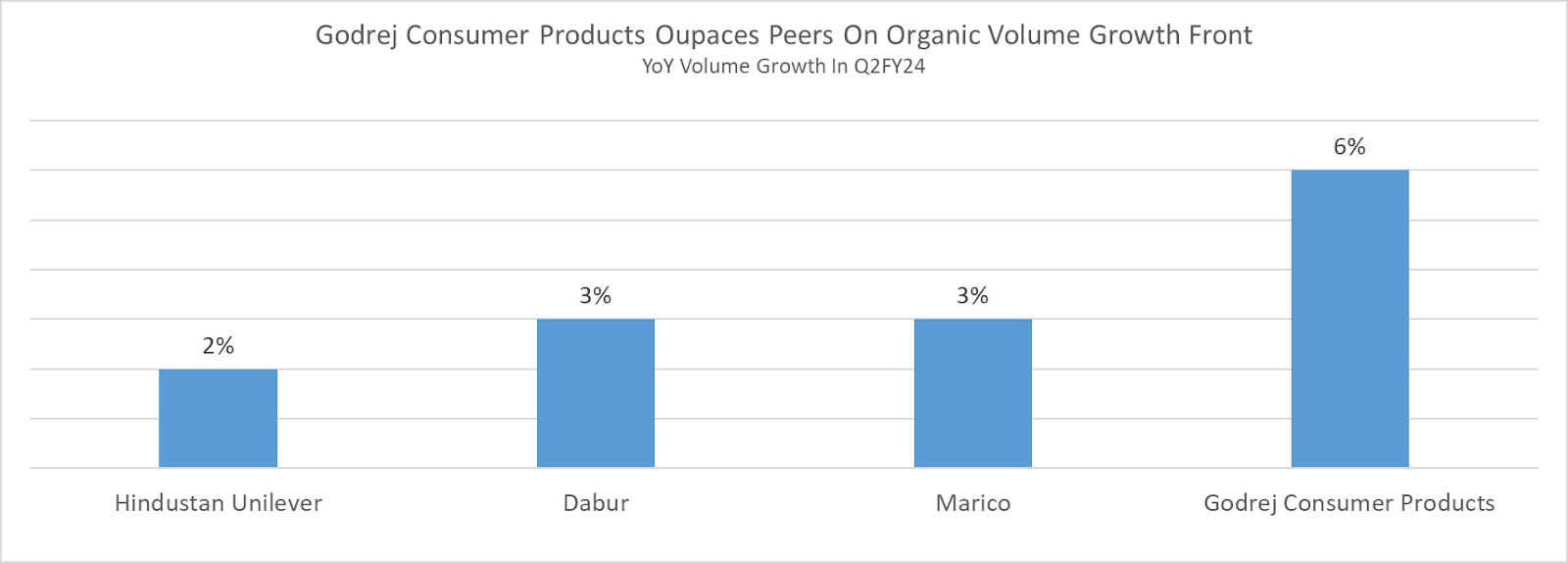

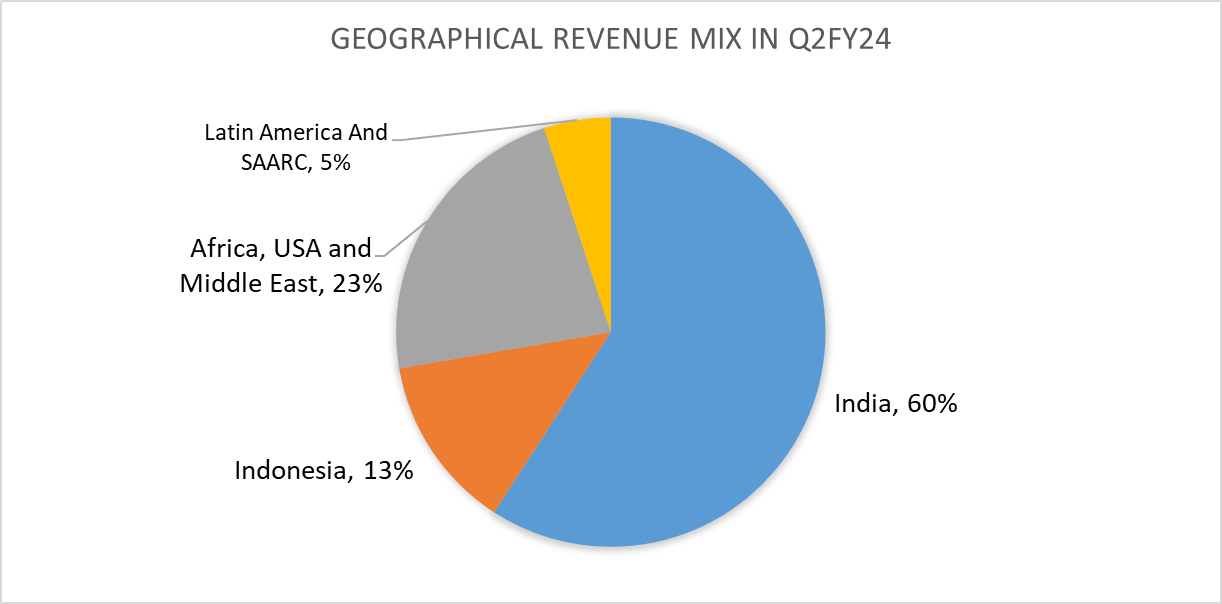

Godrej Consumer Products reported stable September Quarter 2023 supported by both domestic and international markets. The company derives 60% of its revenues from Indian markets and the remaining from Indonesia, Africa, USA, Latin America and SAARC. Godrej Consumer Products Ltd (GCPL) reported volume growth of 10% and organic volume growth of 6% YoY in Q2FY24. Organic volume growth refers to volume growth not attributable to mergers and acquisitions. In the case of GCPL, volume growth of 6% YoY does not include Raymond Consumer Care’s (RCCL) volume growth. Godrej Consumer Products acquired RCCL in April 2023. Still, GCPL is ahead of its peers on the volume growth front in Q2FY24.

Stable September Quarter 2023, Margins To Expand Further

Godrej Consumer Products, makers of HIT and Cinthol reported steady Q2FY24 numbers supported by 10% YoY volume growth across domestic and international markets.

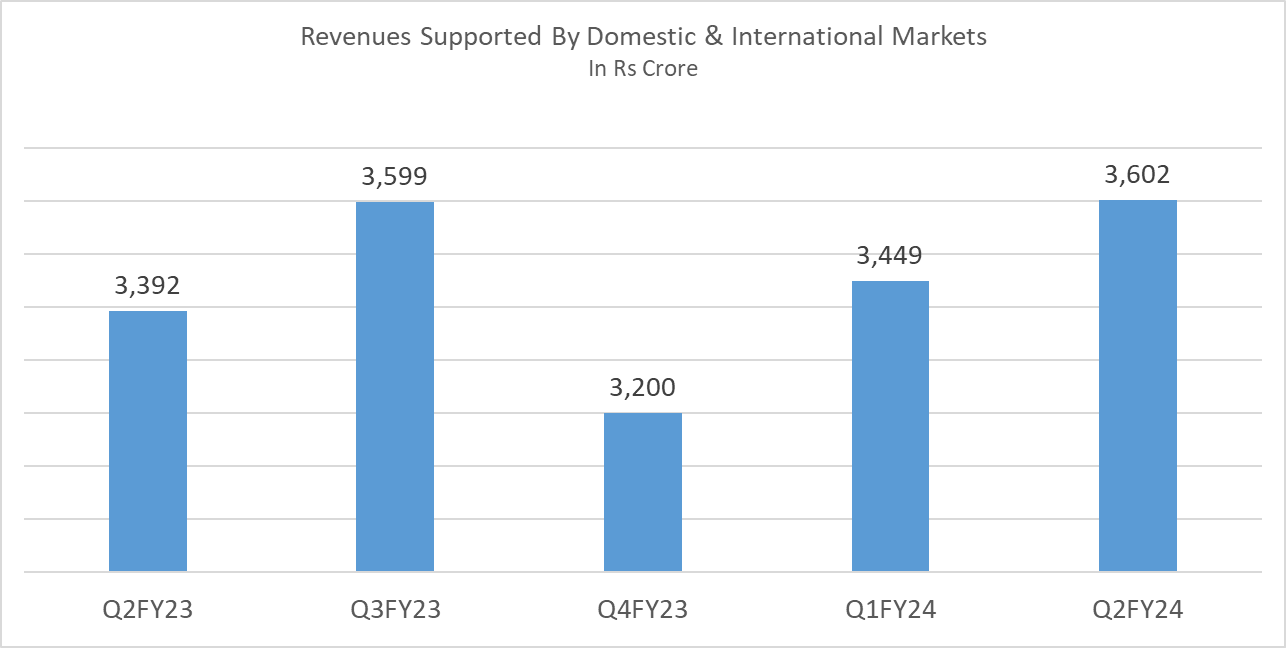

Consolidated revenues grew 6% to Rs 3,602 crore in Q2FY24 compared to Rs 3,392 crore in the same period previous year.

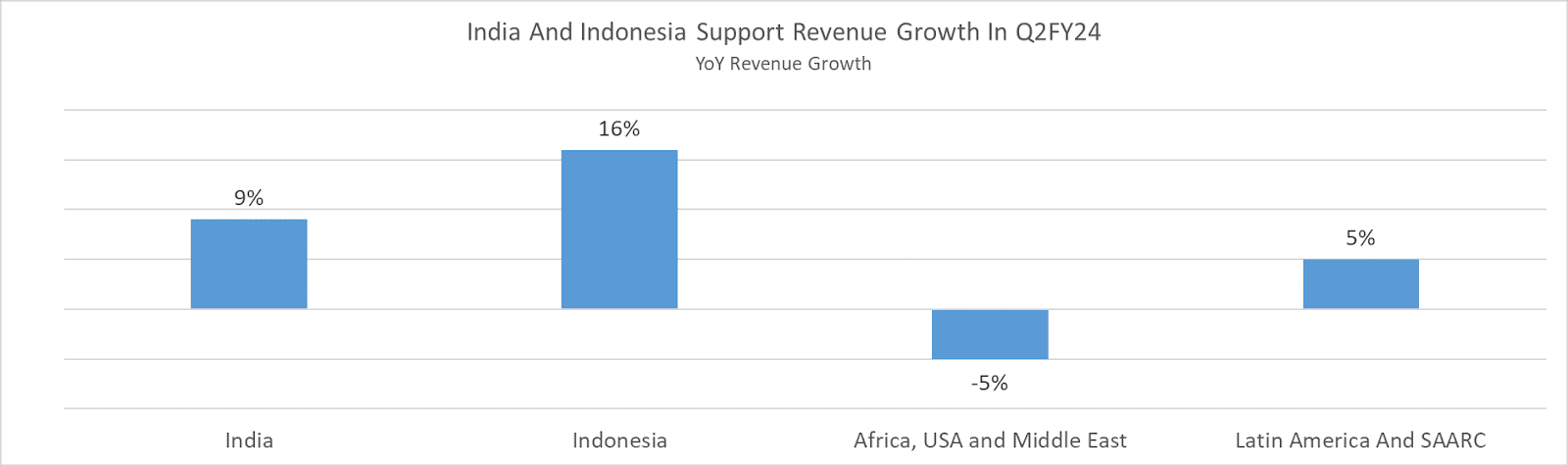

While India reported 9% YoY revenue growth, Indonesia topped with strong double-digit growth of 16% YoY in Q2FY24.

Speaking on September Quarter 2023 results, Sudhir Sitapati, Managing Director and CEO said, “Revenue growth lagged volume growth mainly due to lower prices in personal wash, translation impact in Nigeria and hyperinflation accounting in Argentina.”

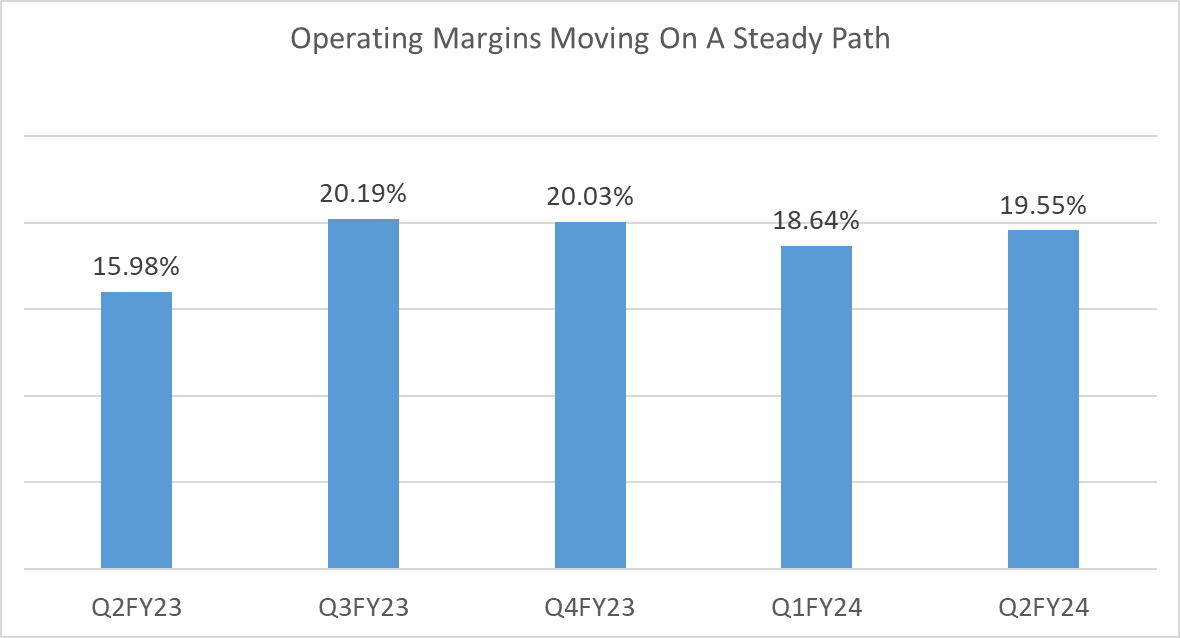

Operating margins came in at 19.55% compared to 15.98%, expansion of more than three percentage points YoY in Q2FY24. According to the management, operating margins are set to improve further supported by GAUM margins which are expected to improve with business organization by Q4FY24. The company is moving its hair fashion business operations in GAUM countries to an asset-light royalty model. “Indonesia margins are also below normative margins, and we think that businesses should improve margins. We also think that there are structural cost savings that are possible in India”, said Sitapati. And the company aims to expand margins despite its hefty media and advertisement & promotion (A&P) spends. A&P expenditure (Rs 366 crore) increased 29% YoY in Q2FY24. GCPL is currently spending 10% of its turnover on A&P.

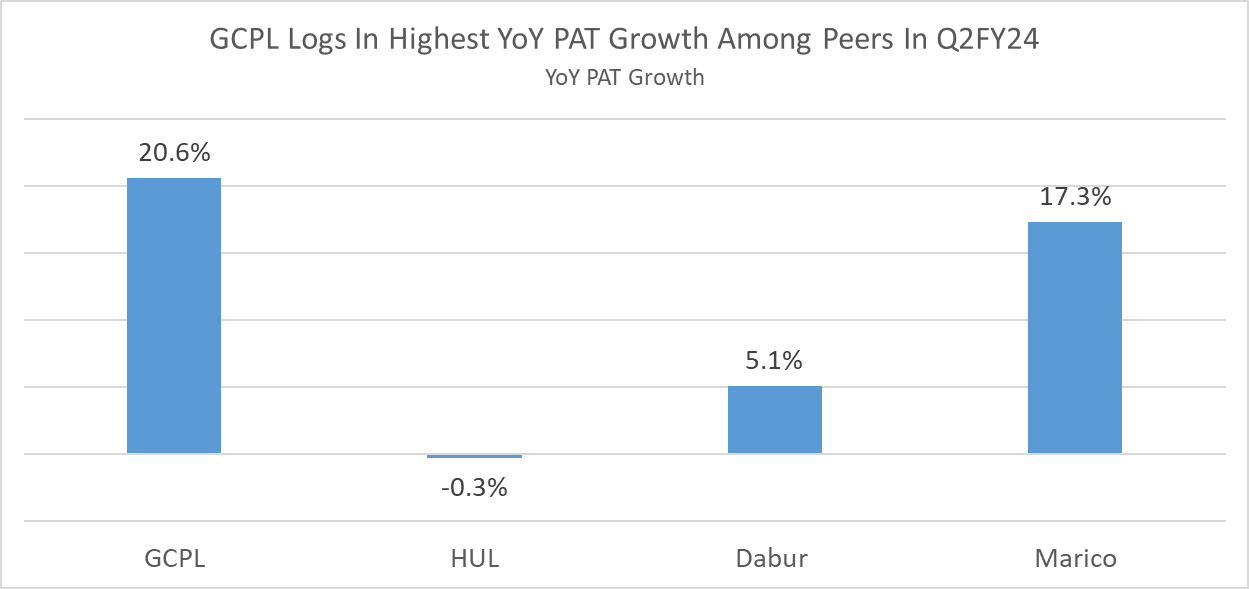

Net profit increased 20% YoY in September Quarter 2023, highest among its close peers. GCPL delivered a net profit of Rs 433 crore in Q2FY24.

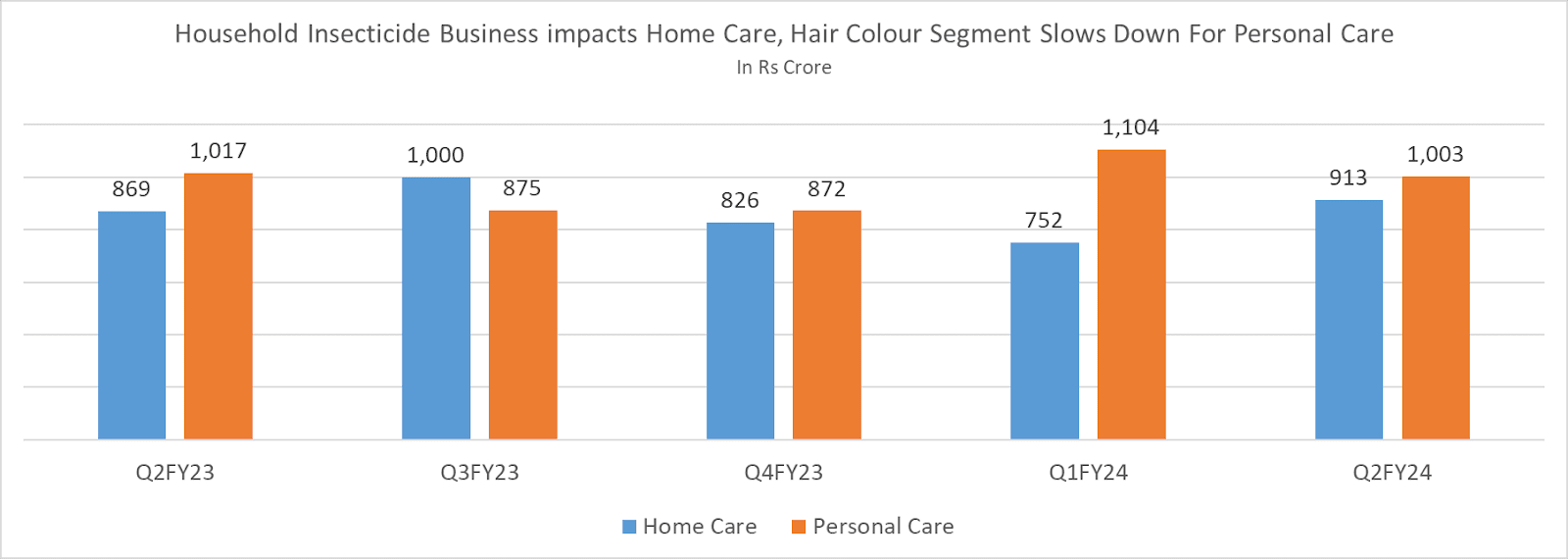

Household Insecticide and Hair Care segments drag growth In Q2FY24

Godrej Consumer Products operates across two main business segments, homecare and personal care. Homecare is segmented into household insecticide (HI) and air fresheners. Personal care comprises personal wash and hair colour businesses. GCPL’s household insecticide business with popular ‘HIT’ and ‘Goodnight’ brands is not doing well for the past two years. As the pandemic fever fear factor faded away from the consumer psyche, household insecticide revenues have stagnated. Another major reason is the highly competitive unorganized incense stick market in India. Incense sticks made from pesticides and chemicals have higher efficacy and are a cheap alternative to popular mosquito repellent brands especially in rural India. In rural regions, incense stocks and coils have higher penetration than liquid vaporizers. According to the management, the month of August witnessed exceptionally dry weather leading to flattish YoY volume growth in September Quarter 2023. The management is aware of consistent muted HI segment performance. “We will come with a structural solution quite soon and we hope to move the category to high single-digit kind of volumes”, said Sitapati. While HI segment underperformed, air fresheners consistently delivered strong double-digit volume and value growth in Q2FY24.

In the personal care segment, personal wash with Cinthol as its popular brand delivered low single-digit volume growth. Magic Handwash continued with its strong double-digit volume growth in September Quarter 2023. Hair care segment reported mid-single volume growth YoY in Q2FY24. Speaking on muted hair care volumes, Sitapati said, “The category usually dips in July during the month of Shravan when consumers in northern and western India do not cut or groom their hair. 2023 was a unique year after 19 years, where a second or Adhik month of Shravan was an added demand dampener.”

Hair care volumes slowed down to mid-single digits in Q1FY24 after five strong quarters. According to the management, the high base of Q1FY23 was a major reason for muted YoY volume growth in June Quarter 2023 performance. And lower Q2FY24 volumes were mainly due to a second additional Shravan month which the management did not forecast, said Sitapati. Investors will be keenly watching the hair care segment performance in the coming quarters along with steps taken by management to revive household insecticide business. And also recently acquired Raymond consumer care business performance.

Erstwhile Raymond Consumer Care business is EBITDA positive

GCPL acquired Park Avenue and Kamasutra brands which constituted FMCG or Raymond Consumer Care (RCCL) business of Raymond Group in April 2023 for Rs 2,800 crore. With this acquisition, GCPL forayed into sexual wellness and deodorant business. Presently, GCPL has completely integrated the RCCL distribution network with itself. This has led to savings of around 400-500 bps of margins, said Sitapati. He further added that business integration has also been completed which has led to reduction of overheads by 70%. According to the management, cost synergies will flow from H2FY24.

Both Park Avenue and Kamasutra brands have strong recall value, but GCPL is pursuing aggressive growth by scaling up media and A&P spends. While RCCL business was doing well in modern trade and ecommerce, rural India was a whitespace for the consumer care business. Currently, the business is witnessing strong incremental sales in rural India through GCPL’s general trade network. “We are also working very closely to devise and create a chemist system, which takes the best of GCPL and RCCL. Most of it is already done, which is a consolidated solid chemist operation for both GCPL and erstwhile RCCL products.”, said Sitapati. After cutting SKUs, inventory and scaling up A&P spends considerably, RCCL business reported sales of Rs 142 crore in September 2023 Quarter and is EBITDA positive. Speaking on erstwhile RCCL business, Sitapati said, “Probably, a few months later, we will know how much advertising and distribution has helped.” Investors are also keenly watching how profitable RCCL business acquisition is going to be.